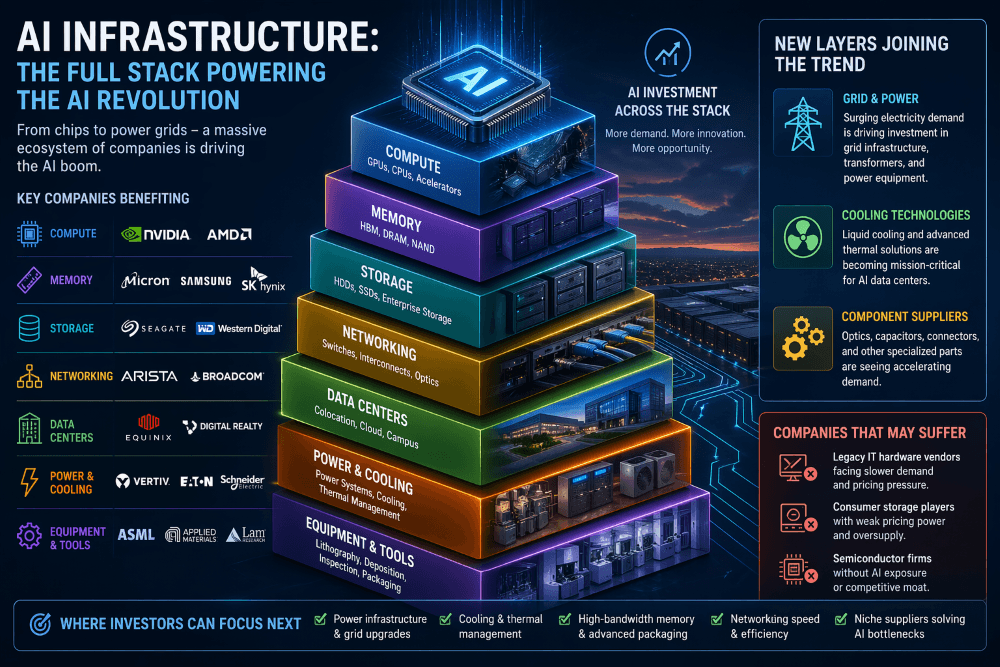

The Rise of AI Infrastructure Stocks

AI infrastructure stocks are no longer a niche trade. They are becoming the backbone of the modern market narrative.

Companies like Intel, Seagate Technology, and Western Digital have been trending upward, but they are just one layer of a much larger system.

The real story is not artificial intelligence itself. It is the physical and digital infrastructure required to support it.

AI Infrastructure Stocks Across the Stack

To understand where this trend is going, you need to see the full stack.

1. Compute: The Engine

At the top sit the compute giants:

- NVIDIA

- Advanced Micro Devices

These companies power AI models. Their chips are essential, but they are only the beginning.

2. Memory and Storage: The Data Layer

AI requires enormous datasets.

That is why companies like:

- Micron Technology

- Samsung Electronics

- SK Hynix

are benefiting alongside storage players like Seagate and Western Digital.

The shift is simple: more AI means more data, and more data needs storage.

3. Networking: The Hidden Bottleneck

Moving data is just as important as storing it.

Key players include:

- Arista Networks

- Broadcom

Without fast networking, AI clusters become inefficient. This layer is quietly outperforming.

4. Power and Cooling: The Constraint Layer

AI data centers consume massive energy.

That’s why companies like:

- Vertiv Holdings

- Eaton

- Schneider Electric

are emerging as critical players.

This is one of the most important shifts: power, not chips, may become the limiting factor.

5. Data Center Real Estate

The physical footprint matters too.

- Equinix

- Digital Realty

These companies are benefiting from surging demand for space and connectivity.

Which Companies May Suffer?

Not every company benefits equally.

Some segments face pressure:

- Traditional IT hardware vendors with no AI angle

- Consumer storage segments with weak pricing power

- Legacy semiconductor firms without AI exposure

In many cases, capital is rotating away from “good enough” businesses into AI-critical infrastructure.

New Layers Still Joining the Trend

AI infrastructure stocks are not done expanding.

The trend is now moving into less obvious areas:

Industrial and Grid Expansion

AI needs electricity, lots of it.

This benefits:

- Grid equipment manufacturers

- Transformer producers

- Utility infrastructure providers

AI data centers are extremely power-hungry. That pushes demand into grid hardware, transformers, and electrical systems.

Core grid and power equipment

- Eaton – electrical systems, data center power distribution

- Schneider Electric – grid + automation + data center integration

- Siemens – grid infrastructure and smart electrification

- ABB – transformers, substations, electrification

Transformer and grid specialists (more direct exposure)

- Hitachi Energy (part of Hitachi) – HVDC, transformers

- GE Vernova – grid equipment and electrification

Utility-scale beneficiaries

- NextEra Energy – power generation tied to data center demand

- Constellation Energy – nuclear + baseload for AI

These names benefit from a simple reality: AI demand is turning electricity into a scarce resource.

Smaller Component Suppliers

Another emerging layer includes:

- Optical component makers

- Thermal management specialists

- Niche semiconductor suppliers

These companies often move later in the cycle, but sometimes with stronger upside.

Cooling & Thermal Management (the silent constraint)

Dense AI racks generate enormous heat. Cooling is becoming mission-critical.

- Vertiv Holdings – liquid cooling, thermal systems

- Trane Technologies – commercial cooling systems

- Carrier Global – data center cooling exposure

- Johnson Controls – smart cooling + infrastructure

This group has already started to outperform, which tells you the constraint is real.

Optical & Networking Components (data movement bottleneck)

As clusters scale, moving data efficiently becomes just as critical as processing it.

- Coherent Corp. – lasers, photonics

- Lumentum Holdings

- Ciena – optical networking gear

- Fabrinet – builds optical modules

These are classic “second-derivative” plays. They tend to move later, sometimes violently.

Memory Supply Chain (HBM and beyond)

High-bandwidth memory is one of the tightest constraints in AI.

- Micron Technology

- SK Hynix

- Samsung Electronics

Upstream enablers (often overlooked)

- KLA Corporation – process control

- Applied Materials – fabrication tools

This is a supply-constrained, pricing-power segment, which is why it keeps attracting capital.

Niche Semiconductor & Connectivity Suppliers

These are the “glue” of AI infrastructure. Not glamorous, but essential.

- Marvell Technology – custom AI silicon + networking

- Monolithic Power Systems – power management chips

- ON Semiconductor – power and sensing

- Amphenol – connectors and interconnects

These companies benefit from every server built, regardless of who wins the AI model race.

A sharper way to think about it

Instead of grouping by industry, think in terms of constraints:

- Power constraint → Eaton, Schneider, utilities

- Heat constraint → Vertiv, Trane

- Data movement constraint → Coherent, Ciena

- Memory constraint → Micron, SK Hynix

- System complexity constraint → Amphenol, Monolithic Power

Wherever you see a bottleneck forming, you’re likely to find pricing power and strong stock performance.

Final perspective

The obvious AI winners were about compute.

This next phase is about what breaks when AI scales.

That’s why these “non-obvious” names matter. They sit exactly where demand is strongest and supply is hardest to expand.

If the trend continues, don’t be surprised if some of these constraint-layer companies become the next leadership group.

The key insight is simple:

The best investments are often found where demand is rising faster than supply can respond.

Are We Seeing Narrowing Leadership?

Not yet.

The trend is still expanding across the stack, but leadership is becoming more selective.

Instead of everything rising together, we are seeing:

- Strong winners within each layer

- Capital flowing to the most critical bottlenecks

- Increasing differentiation between leaders and laggards

This is typical of a mid-cycle expansion, not the end of a trend.

Final Thoughts

AI infrastructure stocks are evolving from a simple story into a complex ecosystem.

The market is no longer asking whether AI will grow. It is asking what will limit that growth.

That shift is where opportunity lies.

Investors who understand the full stack, and especially the emerging constraints, will be better positioned for what comes next.

FAQ

What are AI infrastructure stocks?

AI infrastructure stocks are companies that provide the hardware, software, and physical systems needed to support artificial intelligence, including chips, storage, and data centers.

Which sectors benefit most from AI growth?

Semiconductors, memory, networking, data centers, and power infrastructure are among the biggest beneficiaries.

Are AI infrastructure stocks overvalued?

Some leaders may be expensive, but many second-order and emerging players still offer potential upside.

What is the next big opportunity in AI investing?

Power infrastructure, cooling systems, and grid expansion are emerging as critical and underappreciated areas.

Previous stock market posts