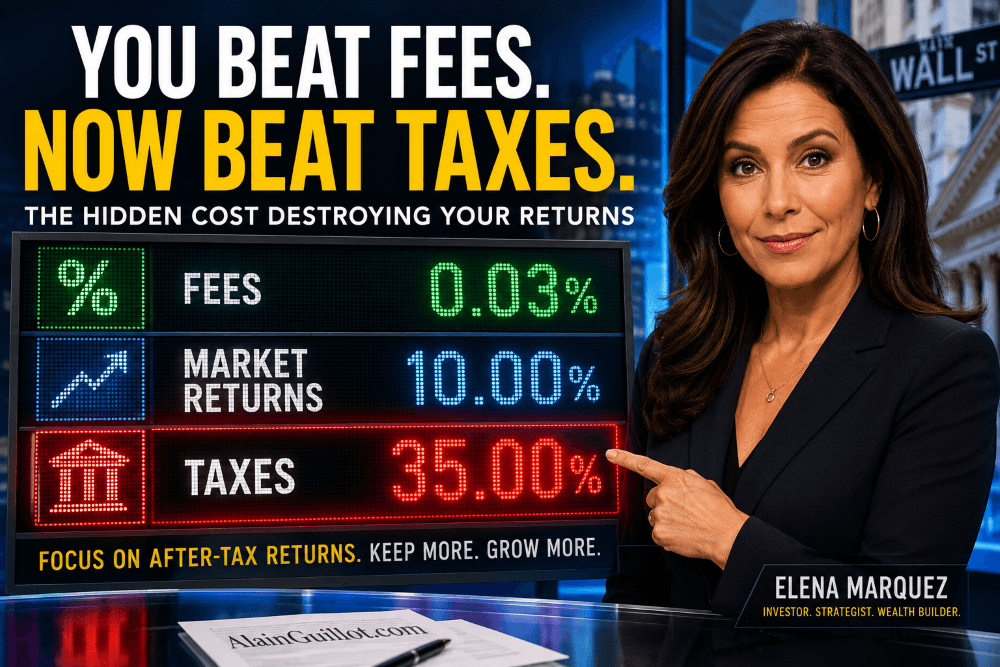

For years, investors fought a war against high investment fees. Thanks to index funds and ETFs, that battle has largely been won. Today, many investors pay less than 0.05% annually in fund expenses.

However, when we focus so mucho on fees, I feel that we are focusing on the wrong thing. At its wose some investment fees can go at about 2% of capital, but something more important to focus on are taxes. For example, taxes on interest income can be as high as taxes on salary or hourly income; that’s a lot.

Tax drag is the reduction in investment returns caused by taxes. While fees have fallen dramatically, taxes continue to quietly erode wealth year after year.

The tragedy is that most investors pay far more attention to fees than taxes, even though taxes often have a much larger impact on long-term returns.

Why Tax Drag Matters

The real danger of tax drag isn’t simply the taxes you pay today.

The real damage comes from losing the ability to compound that money for decades.

Every dollar paid in taxes is a dollar that can no longer earn future returns.

Over a 30-year investing career, this can reduce your final portfolio value by hundreds of thousands or even millions of dollars.

Many investors spend hours comparing expense ratios of 0.03% versus 0.05%, while ignoring investment decisions that create annual tax bills of 15%, 20%, or even more.

That is focusing on pennies while ignoring dollars.

Tax Drag and Dividend Investing

One of the most popular investing strategies on social media is dividend investing.

Investors proudly showcase portfolios generating monthly income from dividends and celebrate every cash distribution.

I believe this strategy is deeply flawed.

1. Dividend Investing Often Produces Inferior Returns

The evidence is overwhelming.

A broadly diversified index fund tracking the S&P 500 has historically outperformed many popular dividend-focused strategies.

Companies that pay high dividends are often mature businesses with fewer opportunities for growth.

Meanwhile, companies that reinvest profits into expansion, innovation, and acquisitions often generate higher long-term shareholder returns.

The goal of investing should be to maximize after-tax wealth, not maximize dividend payments.

2. Dividends Create Immediate Tax Liability

Every dividend distribution creates a taxable event.

Even if you don’t need the money.

Even if you would rather leave every dollar invested.

Even if market conditions make receiving income undesirable.

The government gets paid first, and your portfolio growth suffers.

This constant tax leakage reduces the power of compounding.

3. You Don’t Control When Dividends Are Paid

This is perhaps the most overlooked problem.

When a company decides to distribute cash, you have no choice.

The distribution arrives whether you need the money or not.

Some years you may have significant employment income and already be in a high tax bracket. Receiving additional dividend income during those years can increase your tax burden.

Other years, perhaps after retirement or during a temporary reduction in income, receiving additional cash distributions may actually be beneficial.

The problem is that dividend investors don’t control the timing.

The company does.

By contrast, investors focused on capital appreciation can often choose when to realize gains.

That flexibility can be extremely valuable.

The Power of Broad-Based ETFs

Personally, I prefer broad-based ETFs with very low turnover.

My ideal investment has three characteristics:

- Broad diversification

- Extremely low costs

- Minimal taxable distributions

Many total-market and S&P 500 index ETFs fit this description perfectly.

Because turnover is low, taxes are deferred.

Because taxes are deferred, compounding continues uninterrupted.

Because compounding continues uninterrupted, wealth grows faster.

The formula is simple.

Tax Shelters Are Your Best Friend

Reducing tax drag becomes even easier when you use available tax shelters.

For Americans: Maximize Your Roth IRA

If you live in the United States, make every effort to contribute to a Roth IRA.

The Roth IRA is one of the greatest wealth-building tools ever created.

Qualified withdrawals are tax-free.

Future growth is tax-free.

Capital gains are tax-free.

The longer your investment horizon, the more valuable the Roth becomes.

For Canadians: Maximize Your TFSA

Canadian investors have access to an equally powerful tool: the Tax-Free Savings Account (TFSA).

Investment growth inside a TFSA is completely tax-free.

Withdrawals are tax-free.

Capital gains are tax-free.

For long-term investors, maximizing TFSA contributions should be one of the highest financial priorities.

Consider Capital Gain Harvesting

Most investors understand tax-loss harvesting.

Far fewer understand capital gain harvesting.

If your income falls into a low tax bracket, you may be able to realize gains while paying little or no tax.

This strategy increases your cost basis and can reduce future tax liabilities.

In certain situations, harvesting gains can be just as valuable as harvesting losses.

The key is understanding your tax situation and planning accordingly.

Focus on After-Tax Returns

Investors spent decades obsessing over fees.

Today, the bigger opportunity is minimizing tax drag.

Before buying any investment, ask:

- What are the expected returns?

- What taxes will this investment generate?

- How much control do I have over the timing of those taxes?

The best portfolio is not the one with the highest pre-tax return.

The best portfolio is the one that leaves you with the most money after taxes.

That is the number that ultimately matters.

FAQ

What is tax drag?

Tax drag is the reduction in investment returns caused by taxes on dividends, interest, and capital gains. It reduces the amount of money available for compounding.

Why are dividends less tax-efficient?

Dividends create taxable income whenever they are paid, regardless of whether the investor needs the cash or wants to receive it.

What investments help reduce tax drag?

Broad-market index ETFs with low turnover tend to be among the most tax-efficient investments available.

Should I use a Roth IRA or TFSA?

Yes. If you qualify, maximizing contributions to a Roth IRA in the U.S. or a TFSA in Canada is one of the most effective ways to reduce tax drag and increase after-tax wealth.

Other personal finance blog posts