| 📊 Alain’s Holdings — June 2, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 698.26 | +0.96 | +0.14% |

| QQQ | Invesco QQQ Trust | 746.16 | +3.42 | +0.46% |

| XIU.TO | iShares S&P/TSX 60 ETF | 51.64 | +0.68 | +1.33% |

Records Again — AI Capex Bets

Drive Consecutive Highs

For the second straight session, all three major indexes closed at all-time highs. HPE’s blockbuster earnings and Nvidia’s endorsement of Marvell Technology as the “next trillion-dollar company” kept the AI infrastructure trade roaring — even as Alphabet’s historic $80 billion equity raise rattled mega-cap tech.

Index Close

S&P 500

7,609.78

▲ +0.13%1st Close >7,600

Nasdaq Composite

27,093.90

▲ +0.03%Record Close

Dow Jones

51,307.79

▲ +0.45% +228.91 ptsRecord Close

Russell 2000

2,931+

▲ +0.90%Market Snapshot

Notable Movers

📈 Winners

📉 Losers

What Happened Today

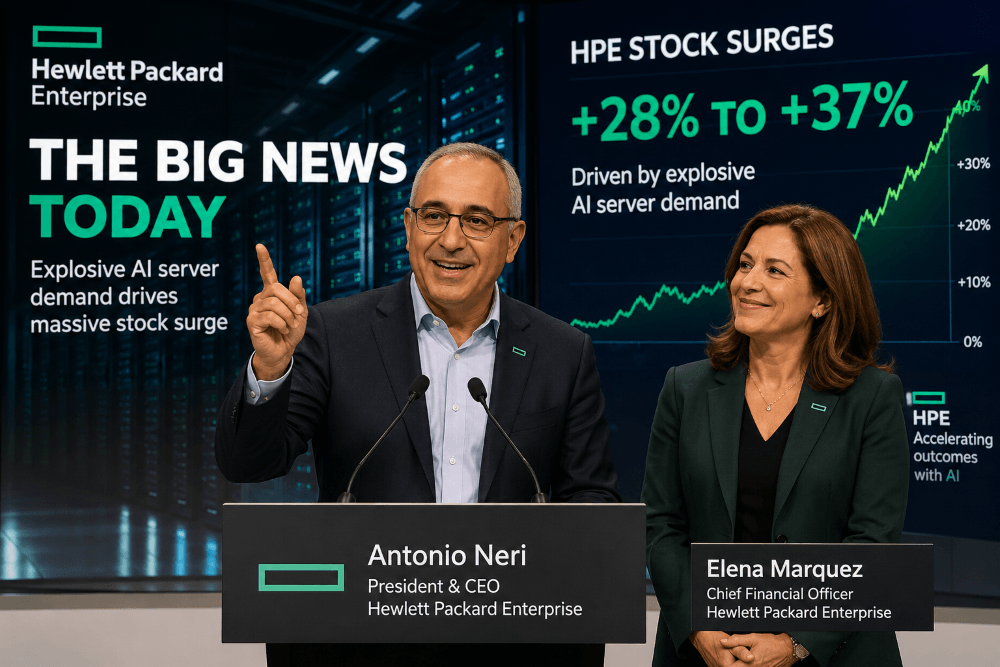

HPE delivered the biggest earnings beat in years. Hewlett Packard Enterprise reported fiscal Q2 adjusted EPS of $0.79 — obliterating the $0.54 consensus — on record revenue of $10.68 billion versus a $9.74 billion estimate. The company pulled its long-term financial targets forward by two years, signalling explosive AI server demand. Shares surged approximately 25–26%, their biggest single-day gain since the company’s 2015 separation from HP. CEO Antonio Neri described the quarter as a turning point for HPE’s position in the AI infrastructure race.

Nvidia anointed Marvell at Computex. On stage in Taipei, Nvidia CEO Jensen Huang declared Marvell Technology could be “the next trillion-dollar company,” sending shares rocketing between 25% and 32% in one of the chip sector’s most dramatic single-session moves in recent memory. The endorsement underscored Marvell’s growing role in custom AI silicon and networking for hyperscale data centers.

Alphabet surprised markets — but not pleasantly. Google’s parent announced it would raise $80 billion through equity offerings — the largest such raise Wall Street has ever seen — to fund its AI infrastructure buildout. Berkshire Hathaway committed $10 billion to the round, a notable vote of confidence. But shares fell roughly 4% on dilution fears and questions about the scale of AI capital expenditure. The announcement reignited the AI-replacement debate across software stocks, sending ServiceNow, Salesforce, and Atlassian lower after their big Monday gains.

Generac Holdings gained 9% after securing a contract to supply backup power generators for a hyperscale operator’s data center network — a direct beneficiary of the AI buildout energy demand theme. Dollar General beat Q1 expectations and raised its profit outlook, with shares climbing on signs that value-conscious consumers remain resilient despite inflation.

Geopolitics remained a mixed signal. Oil pulled back modestly from Monday’s spike — Brent fell toward $93 — after President Trump reaffirmed on Truth Social that U.S.–Iran indirect talks are continuing “at a rapid pace,” partially offsetting fears of prolonged conflict. The Russell 2000 outperformed large caps with a +0.90% gain, suggesting some broadening of the rally beyond mega-cap AI plays.

📊 Economic Data: JOLTS — April 2026

The Bureau of Labor Statistics reported 7.6 million job openings in April — an increase from March’s revised 6.9 million — pointing to a still-resilient labor market heading into Friday’s critical May Nonfarm Payrolls report. Hires edged down to 5.1 million, and total separations held steady at 5.0 million. The “low hire, low fire” dynamic the Fed has been watching continues to define the employment picture.

What to Watch the Rest of This Week

- ADP Private Payrolls (Wednesday): The warm-up act before Friday — consensus expects modest job creation consistent with the “slow-burn” labor market of 2026.

- May Nonfarm Payrolls (Friday): The week’s main event. Unemployment expected to hold at 4.3%. Any wage surprise could shift Fed rate-cut expectations materially.

- Alphabet’s $80B raise: Watch how markets digest the dilution and whether other mega-cap tech names follow suit with large capital raises.

- Iran–U.S. diplomacy: Oil prices remain the swing factor. Trump’s “rapid pace” comment cooled crude on Tuesday; fresh escalation could reverse that quickly.

- Breadth vs. concentration: The Russell 2000’s +0.90% outperformance hints at possible broadening. Sustained breadth would be a bullish sign; another narrow AI-only rally would warrant caution.

Other Stock Market blog posts