When discussing personal responsibility and poverty, conversations often become polarized. Some people argue that poverty is entirely the result of bad luck or unfair systems, while others insist that individuals alone are responsible for their financial circumstances.

The truth is more nuanced.

Some people experience poverty because of circumstances completely beyond their control. A serious illness, a disability, the loss of a job during a recession, domestic violence, or a natural disaster can quickly push an otherwise responsible person into financial hardship. Those individuals deserve compassion and assistance while they get back on their feet. We ofter refer to those people as the deserving poor and we want to help them.

At the same time, there are people who don’t want to help themselves, we call them the underservig poor, they are poor because of their own decisions or behavior. Historically, these are people who are:

- Able to work but unwilling to do so.

- Habitually unemployed despite available opportunities.

- Spending money irresponsibly.

- Engaging in criminal activity instead of lawful employment.

- Persistently abusing alcohol or drugs (though modern perspectives often treat addiction as a medical condition).

- Having kid to claim government assistance

- Claiming mental health issues when they are perfectly fine

For this group are refered to as the Undeservign Poor and assistance should be limited because it may encourage dependency or discourage work.

| Situation | Traditionally classified as |

|---|---|

| An elderly retiree with no savings | Deserving poor |

| A construction worker laid off during a recession | Deserving poor |

| A family whose home was destroyed by a flood | Deserving poor |

| A child living in poverty | Deserving poor |

| Refusing Available Work: Able-bodied individuals who chose not to work, often labeled historically as “sturdy beggars,” “vagrants,” or “idlers.” | Underserving poor |

| Substance Abuse: Spending resources on alcohol or drugs rather than basic needs or family support | Underserving poor |

| Criminal or Anti-Social Behavior: Engaging in petty theft, gambling, scams, or street hustling instead of traditional employment | Underserving poor |

| Mismanagement of Funds: Expending money on non-essential goods or entertainment while relying on community charity for survival | Underserving poor |

| “Welfare Queen” having lots of kids to collect government child assistance | Underserving poor |

Most of the time long-term poverty can be reduced—or even avoided—through a series of ordinary, practical decisions. These decisions are not glamorous, nor do they guarantee wealth. But over time, they dramatically increase the odds of achieving financial stability.

Likewise, government policies can either create opportunities or erect unnecessary barriers. Good public policy should make it easier for people to become self-sufficient rather than unintentionally trapping them in dependency.

There is no reason to be poor in the U.S. or Canada

There is no permanent reason to remain stuck in poverty in the U.S. or Canada, as even an individual with very little formal education can readily secure a starting position in the massive retail, hospitality, or modern gig economy sectors.

Everyday opportunities abound for those willing to get a foot in the door—whether it is stocking shelves at a local Walmart, Target, or neighborhood supermarket; working as a server, busboy, or kitchen helper in the ever-hiring restaurant industry; or launching a flexible schedule as an Uber driver or DoorDash courier.

Beyond these, fields like commercial cleaning, warehousing and fulfillment center labor, construction labor, and security services consistently hire with minimal prerequisites or prior work experience. Once a person secures an entry-level foothold, the trajectory of their income depends entirely on personal drive, reliability, and continuous self-improvement.

While the first five years can be undoubtedly difficult, consistently showing up on time, executing duties reliably, and actively taking courses or learning new skills outside of work hours provides a clear, actionable roadmap to climbing the economic ladder.

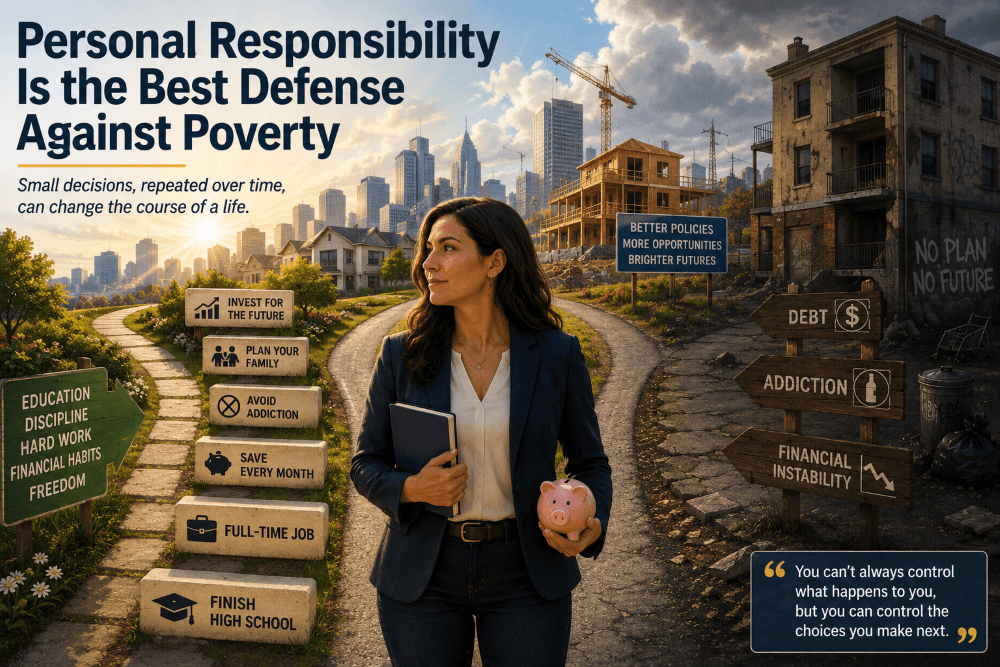

Personal Responsibility and Poverty: Six Habits That Matter

There is no magic formula for becoming wealthy. However, decades of research consistently point toward several habits that significantly improve a person’s chances of avoiding chronic poverty.

1. Finish High School

Education is one of the strongest predictors of future earnings.

A high school diploma is often the minimum requirement for many entry-level jobs. More importantly, completing high school demonstrates perseverance, responsibility, and the ability to finish long-term goals.

Not everyone needs a university degree. Many people build excellent careers through skilled trades, apprenticeships, military service, entrepreneurship, or technical training. But completing high school remains an important foundation.

2. Maintain Full-Time Employment

Having a steady income changes almost every aspect of a person’s financial life.

Even if the first job is not ideal, consistent employment helps people:

- Build work experience.

- Develop professional skills.

- Earn promotions.

- Establish good references.

- Increase future earning potential.

Many successful careers begin with jobs that are far from glamorous. Every honest job teaches valuable lessons about discipline, customer service, teamwork, and reliability.

Many CEOs started at the lowest position in their low level job. Examples are:

- Mary Barra who started checking fender panels at General Motors at age 18

- Doug McMillon — Walmar; who took a summer job as a teenager loading delivery trucks at a Walmart distribution center to help fund his college education.

- Chris Rondeau — Planet Fitness; who started working part-time at the very first Planet Fitness location in New Hampshire when he was a 19-year-old college student.

Waiting for the “perfect job” often delays progress. Starting somewhere is usually better than standing still.

3. Plan Parenthood Carefully

Raising children is one of life’s greatest joys, but it is also one of its greatest responsibilities.

Children deserve stable homes where parents can provide emotional support, financial security, and a safe environment.

For many couples, delaying parenthood until they have established a stable relationship and sufficient financial resources reduces stress for both parents and children.

Life rarely follows a perfect script, and many wonderful parents successfully raise children under difficult circumstances. Nevertheless, thoughtful family planning generally improves long-term outcomes for everyone involved.

Having a child when you are struggling financially can be chalked up to a mistake or a strong emotional desire, but continuing to have a second or third child under those conditions is simply reckless judgment.

4. Avoid Addiction

Most people can enjoy a glass of wine with dinner, a beer while watching a hockey game, or an occasional cannabis edible without it becoming a problem. The issue is not moderate consumption; it is addiction.

When alcohol, drugs, or gambling begin to control a person’s life, the financial consequences can be devastating. Addiction often leads to:

- Lost employment.

- Damaged relationships.

- Legal problems.

- Poor physical and mental health.

- Mounting debt.

Breaking an addiction is incredibly difficult, and many people need professional treatment and the support of family and friends. There should be no shame in seeking help. Recovery is possible, and every step toward sobriety is also a step toward greater financial stability.

I have no sympathy for drug addicts who choose this path. They should be at the end of the line for financial help. In California, millions in aid to drug users have failed to solve the crisis — the problem persists as bad as ever.

5. Build the Habit of Saving

One of the biggest financial myths is that only wealthy people can save money.

The truth is that saving is first and foremost a habit.

Early in my life, I worked as a janitor while attending school full-time. I wasn’t earning much, yet I made it a priority to save $25 every month.

Twenty-five dollars wasn’t enough to change my life overnight. But it taught me something far more valuable than the money itself: the discipline of paying myself first.

That habit stayed with me as my income increased. Later, I saved hundreds of dollars each month. Eventually, I invested those savings, and over the years they compounded into meaningful wealth.

Not everyone can save the same amount. Someone supporting a family on minimum wage faces different challenges than someone earning a professional salary. But whenever possible, even small, consistent savings create a financial cushion that can prevent minor setbacks from becoming major crises.

The goal is not perfection. The goal is to develop a habit that grows stronger over time.

6. Think Long Term

Many financial decisions involve a trade-off between today’s comfort and tomorrow’s opportunities.

Learning a new skill instead of spending hours scrolling through social media.

Saving part of a tax refund instead of spending all of it immediately.

Working overtime for a period to eliminate high-interest debt.

Investing regularly instead of trying to get rich quickly.

None of these decisions are exciting. They simply reflect a long-term mindset.

People who consistently ask, “How will this decision affect me five years from now?” often make better financial choices than those who focus only on immediate gratification.

Government Policies Also Matter

Personal responsibility is only part of the equation.

Public policy can either expand opportunities or make economic mobility unnecessarily difficult.

Housing Affordability

In many North American cities, restrictive zoning rules limit the construction of new housing.

When supply cannot keep up with demand, housing becomes more expensive. Young families, students, and lower-income workers often bear the greatest burden.

Policies that encourage more housing construction can make home ownership and renting more affordable without requiring permanent government subsidies.

Occupational Licensing

Some occupations require licensing to protect public safety. Doctors, nurses, pilots, and electricians perform work where high professional standards are essential.

However, licensing requirements have expanded into many occupations where the public benefits are less clear.

Examples of riduculous occupational licenses are:

- Hair Braiders: In several states and provinces, practicing traditional African hair braiding—which involves no cutting, chemicals, dyes, or heat—historically required a full, expensive cosmetology license.

- Interior Designers: In places like Florida, Nevada, or Washington D.C., becoming a registered interior designer can require up to six years of combined higher education and supervised apprenticeship, plus passing a rigorous multi-part exam.

- Florists: To become a retail florist, aspiring business owners must pay a fee and pass a state-administered exam.

In some cases, workers who are fully qualified in one province or state must repeat costly licensing processes simply because they moved across a border.

Reducing unnecessary barriers while maintaining appropriate safety standards would make it easier for skilled workers to pursue new opportunities and fill labor shortages.

Avoiding Benefit Cliffs

A well-designed social safety net should provide temporary assistance while encouraging people to become financially independent.

Unfortunately, some benefit programs create what economists call a benefit cliff. As people begin earning more income, they may lose housing assistance, childcare subsidies, or other benefits so quickly that accepting additional work leaves them little better off financially.

Good policy should reward work.

Programs that phase out benefits gradually rather than abruptly can encourage people to pursue promotions, work additional hours, or accept higher-paying jobs without fear of immediately losing critical support.

Compassion and Responsibility Can Coexist

Public debates about poverty often fall into two extremes.

One side argues that poverty is almost entirely caused by unjust systems. The other argues that every person is solely responsible for his or her financial circumstances.

Reality is usually somewhere in between.

Some people face hardships that no amount of personal responsibility could have prevented. A child born into poverty, someone diagnosed with cancer, or a worker laid off because an entire factory closes deserves understanding and, when appropriate, public assistance. A compassionate society should not abandon people facing circumstances beyond their control.

At the same time, we should not ignore the fact that our daily decisions matter. Completing an education, working consistently, avoiding addiction, planning parenthood responsibly, living below our means, and saving regularly are habits that dramatically improve the odds of financial stability.

Recognizing the importance of personal responsibility is not about blaming people. It is about empowering them.

Helping Those Who Need It Most

No society has unlimited resources.

Governments and charities must make difficult decisions about how to allocate limited funds. In my view, assistance should first go to those who genuinely cannot support themselves because of age, disability, illness, temporary economic hardship, or other circumstances beyond their control.

At the same time, social programs should be designed to encourage independence whenever possible. The goal of assistance should be to help people regain their footing, not to create situations where earning more income leaves someone worse off because of abrupt benefit losses.

A successful anti-poverty strategy combines two principles:

- A strong safety net for people facing genuine hardship.

- Policies that encourage education, employment, entrepreneurship, and financial independence.

These principles are complementary, not contradictory.

And of course, those who don’t help themselves, like the drug addicts and the walfare queens, should not get any help at all.

Final Thoughts

There is no guaranteed path to wealth.

Life can be unfair. Bad things happen to good people. Luck—both good and bad—plays a role in every life.

But we should not underestimate the power of ordinary decisions repeated over many years.

Finishing school.

Showing up for work.

Avoiding destructive habits.

Saving a little every month.

Investing for the future.

Planning major life decisions carefully.

None of these actions will make someone an overnight millionaire. Yet together, they substantially increase the likelihood of avoiding chronic poverty and building a more secure future.

Public policy matters. Economic opportunity matters. Personal responsibility matters.

When all three work together, individuals, families, and society are more likely to prosper.

Frequently Asked Questions

Can personal responsibility eliminate poverty?

No. Some people experience poverty because of illness, disability, economic recessions, family circumstances, or other factors beyond their control. However, personal responsibility can significantly reduce the risk of long-term poverty for many people.

What are some habits that reduce the risk of poverty?

Research consistently shows that completing high school, maintaining steady employment, avoiding addiction, planning parenthood responsibly, and developing a habit of saving improve long-term financial outcomes.

What are some habits that increase the risk of poverty?

Being able to work but unwilling to do so.

Being Habitually unemployed despite available opportunities.

Spending money irresponsibly.

Engaging in criminal activity instead of lawful employment.

Persistently abusing alcohol or drugs (though modern perspectives often treat addiction as a medical condition).

Being a walfare queen.

Does government policy affect poverty?

Yes. Housing regulations, occupational licensing, taxation, education, and the design of social benefit programs all influence economic opportunity and upward mobility.

Is saving money worthwhile if I can only save a small amount?

Absolutely. Small, consistent savings build financial resilience and develop lifelong financial habits. Over time, those habits often matter more than the initial dollar amount.

Other Personal Development Posts

Leave a Reply