For years, I have been telling friends: “Just buy the market, don’t waste your time with individual stocks.”

The problem is that most of them don’t know what I am talking about, and to be honest, sometimes I don’t know what I am talking about either. Because not all “markets” are created equal. They don’t behave the same way, and they aren’t all appropriate for every investor.

Today, I will talk about the three primary markets people discuss, how each one behaves, and how a regular Canadian can choose between them. Those three markets are:

- QQQ, the

- S&P 500, and the

- TSX index.

Once you understand the differences, you will be able to judge which is a better fit for your portfolio and where they should be placed.

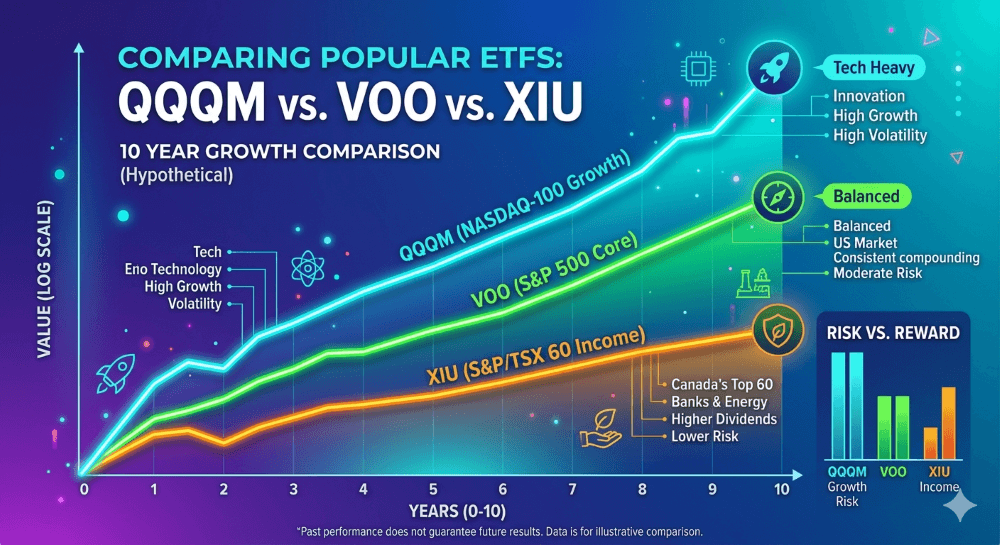

Higher Returns Always Come With Higher Risk

If we stack our three indexes on a risk-return basis, this is what we get:

- QQQ has the highest returns and the highest risk.

- The S&P 500 is less risky and has lower returns than QQQ.

- The TSX has lower returns than the S&P 500 but offers different sector exposure.

My preferred ETFs to buy these indexes are:

- For QQQ: I like an ETF called QQQM.

- For the S&P 500: I like VOO.

- For the Canadian TSX: I like XIU.

For your information, there are different ETF which cover the same indexes. I like the above mentioned because they have low management fees, they are highly liquid, and they have a good reputation.

To give you an idea of the difference in total returns for these three investments over the past 10 years (approximate):

- QQQM (via QQQ): ~+430% to +470%

- Vanguard S&P 500 ETF (VOO): ~+220% to +250%

- iShares S&P/TSX 60 Index ETF (XIU): ~+90% to +120%

But don’t be seduced by higher returns if you cannot withstand drops of 30–35%.

What’s Inside These Different Investments?

These indexes put a magnifying glass on different parts of the economy.

QQQM: The Growth Machine

QQQM is a concentrated bet on technology and innovation.

- Heavy in tech (Apple, Microsoft, Nvidia).

- Minimal exposure to banks or energy.

- Low dividends, high reinvestment.

This is why the returns are high; most of these companies’ business models are scalable globally. But be careful: in a single year, the QQQ was down 32.58%. You need a strong stomach to tolerate a drop of that magnitude.

VOO: The S&P 500 Standard

The S&P 500 is composed of the 500 largest corporations in the U.S. The risk is lower than QQQM because it is diversified across many industrial sectors.

- Annualized return: About 14%.

- Highest annual return: About 31%.

- Lowest annual return: About -18%.

XIU: The TSX for Canadian Patriots

XIU is composed of the 60 biggest Canadian companies.

- Dominated by banks, oil, and mining.

- Higher dividend yield than the U.S. indexes.

- Lower long-term growth potential.

Risk vs. Reward Table

| Index | Returns | Risk | Role |

| QQQ | Highest | Highest | Aggressive Growth |

| S&P 500 | Strong | Moderate | Core Portfolio |

| TSX | Lower | Cyclical | Income & Diversification |

Summary: QQQ makes you rich faster (and scares you more); the S&P 500 makes you rich steadily; the TSX pays you while you wait.

How Should a Canadian Investor Use This Information?

In Canada, we have three main investment “buckets” treated differently for tax reasons: TFSA, RRSP, and Non-registered accounts.

1. TFSA (Tax-Free Savings Account)

Everything in this account grows tax-free. This is the place for your highest-return investments. If you make a 100% return, it is 100% tax-free.

- Best for: QQQM or high-growth individual stocks. You keep all capital gains; $0 goes to the government.

2. RRSP (Registered Retirement Savings Plan)

Capital gains and dividend income are tax-deferred until you withdraw the money. Furthermore, there is no U.S. withholding tax on dividends in an RRSP. Normally, the IRS imposes a 15% tax on dividends paid to non-residents, but the Canada-U.S. tax treaty waives this for the RRSP.

- Best for: VOO (S&P 500) or any U.S. dividend-paying stocks.

3. Non-Registered Account (Taxable)

Once you hit your TFSA and RRSP contribution limits, you use a regular investment account. In Canada, domestic dividends receive favorable tax treatment through the Dividend Tax Credit.

- Best for: XIU (TSX Index) or Canadian bank stocks that pay regular quarterly dividends

Summary

- TFSA → QQQ / Growth stocks (Maximize tax-free gains).

- RRSP → S&P 500 / U.S. equities (Avoid U.S. withholding tax).

- Non-registered → Canadian dividend stocks (Utilize Dividend Tax Credit).

Final Thought: Stop Looking for the “Best” Index

There is no single “best” index. There is only the one that matches your risk tolerance, time horizon, and emotional discipline. QQQ will outperform until it doesn’t. The TSX will lag until commodities surge. The S&P 500 will quietly compound in the background. The real edge isn’t picking the winner—it’s understanding why each one wins at different times and positioning yourself accordingly.

Frequently Asked Questions (FAQ)

Which is better for Canadians: VOO or XIU? It depends on your goal. VOO (S&P 500) offers higher historical growth and U.S. tech exposure, while XIU (TSX 60) offers higher dividends and stability through Canadian banks and energy.

Why should I hold U.S. stocks in my RRSP instead of my TFSA? While both are great, the RRSP is uniquely exempt from the 15% U.S. withholding tax on dividends. If you hold a U.S. dividend-payer in a TFSA, the IRS takes 15% before you see it.

Is QQQM the same as QQQ? Essentially, yes. They track the same index (Nasdaq-100), but QQQM has a lower management fee, making it better for long-term “buy and hold” investors.

What is the “Dividend Tax Credit” for Canadians? It is a tax incentive that reduces the amount of tax you pay on dividends received from taxable Canadian corporations, making the TSX very attractive for non-registered accounts.

Previous stock market posts