| 📊 Alain’s Holdings — June 3, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 693.36 | -4.90 | -0.70% |

| QQQ | Invesco QQQ Trust | 744.21 | -1.95 | -0.26% |

| XIU.TO | iShares S&P/TSX 60 ETF | 51.19 | -0.45 | -0.87% |

The Record Streak Snaps —

Geopolitics Trumps AI

After two consecutive all-time highs, markets pulled back sharply on Wednesday as Iran launched missiles at Kuwait and Bahrain and the U.S. responded with strikes on Qeshm Island. Oil spiked back toward $98. The selloff hit every sector — but Broadcom posted a staggering earnings beat after the bell, setting up tomorrow for a potential reversal.

Index Close

S&P 500

~7,553

▼ −0.74%Nasdaq Composite

~26,851

▼ −0.89%Dow Jones

~50,689

▼ −1.21%Russell 2000

~2,896

▼ −1.25%Market Snapshot

Notable Movers

📈 Bucking the Trend

📉 Under Pressure

What Happened Today

The record streak ends at two. After back-to-back all-time highs on Monday and Tuesday, all four major indexes closed in the red on Wednesday. The Dow dropped more than 1.2% — its worst day in weeks — and the Russell 2000 fell 1.25%, erasing the small-cap gains from the prior session. Communications, financials, and technology were the hardest-hit sectors.

Iran escalated significantly overnight. Iran launched missiles targeting Kuwait and Bahrain, damaging infrastructure and killing at least one person, according to foreign ministry reports. The U.S. military responded with strikes on Iran’s Qeshm Island and targeted oil tankers headed for Iranian ports, per CNN and U.S. military sources. Israeli Prime Minister Netanyahu added to the tension, suggesting in a CNBC interview that Israel could strike Iran again. The confrontation sent oil spiking — Brent crude approached $98 and WTI crossed $96 — and crushed the ceasefire optimism that had partially buoyed markets on Tuesday.

The S&P 500’s nine-day winning streak came under threat. The index had rallied nearly 20% over nine weeks — a historic surge — and Wednesday’s selling reflected a broader repricing of geopolitical risk rather than any fundamental shift in the AI thesis. The Federal Reserve’s Beige Book, released midday, noted that inflation was rising “at a moderate to strong pace” due to the Iran conflict, while the labor market “showed little to no change” across most regions.

Software names continued their rotation-driven slide. ServiceNow, CrowdStrike, and other cloud software stocks fell further as investors debated whether Alphabet’s massive $80 billion AI infrastructure raise — and its AI-replacement implications — changes the software landscape. The whipsaw across software this week underscores the market’s uncertainty about who wins and who loses as AI spending accelerates.

🔆 After-the-Bell Spotlight

Broadcom Delivers a Jaw-Dropping Beat

After the close, Broadcom reported fiscal Q2 revenue of $22.2 billion — up 48% year over year — beating consensus of $22.1B. AI semiconductor revenue hit $10.8 billion, up 143% year over year and above the company’s own $10.7B forecast. Free cash flow reached $10.3 billion (46% of revenue). The stunner was the Q3 outlook: Broadcom guided for $29.4 billion in revenue — up 84% year over year — shattering the Street’s $23B estimate. CEO Hock Tan said AI semiconductor revenue is expected to grow over 200% year over year in Q3. Shares jumped ~4.7% in after-hours trading, pointing toward a green open for the broader chip sector on Thursday.

📊 Economic Data: ADP Private Payrolls — May 2026

ADP reported that the U.S. private sector added 122,000 jobs in May — a solid, steady print that neither alarmed nor excited markets. It suggests the labor market remains intact heading into Friday’s marquee Nonfarm Payrolls report. The consensus for Friday’s NFP is approximately 130,000–140,000 new jobs, with the unemployment rate expected to hold at 4.3%.

What to Watch Tomorrow & Friday

- Broadcom aftermath (Thursday): AVGO’s $29.4B Q3 guide should lift the chip sector at the open. Watch whether the broader market follows or whether geopolitical concern overrides the AI tailwind again.

- Iran–U.S. escalation: Wednesday’s missile exchanges mark a significant step up in hostilities. Oil near $98 and approaching $100 will dominate headlines. Any Strait of Hormuz threats could trigger a much sharper market reaction.

- CrowdStrike & Veeva earnings (Thursday morning): Both report post-close Wednesday. CRWD will be a key read on enterprise cybersecurity spending, while Veeva tests healthcare SaaS resilience.

- May Nonfarm Payrolls (Friday, 8:30 AM ET): The week’s main event. A strong number could push back Fed rate-cut expectations; a miss could accelerate them. Markets are walking a tightrope between AI optimism and macro uncertainty.

- Beige Book signal: Inflation rising at a “moderate to strong pace” due to war is a concern the Fed cannot ignore. If oil stays near $100, the summer inflation picture changes materially.

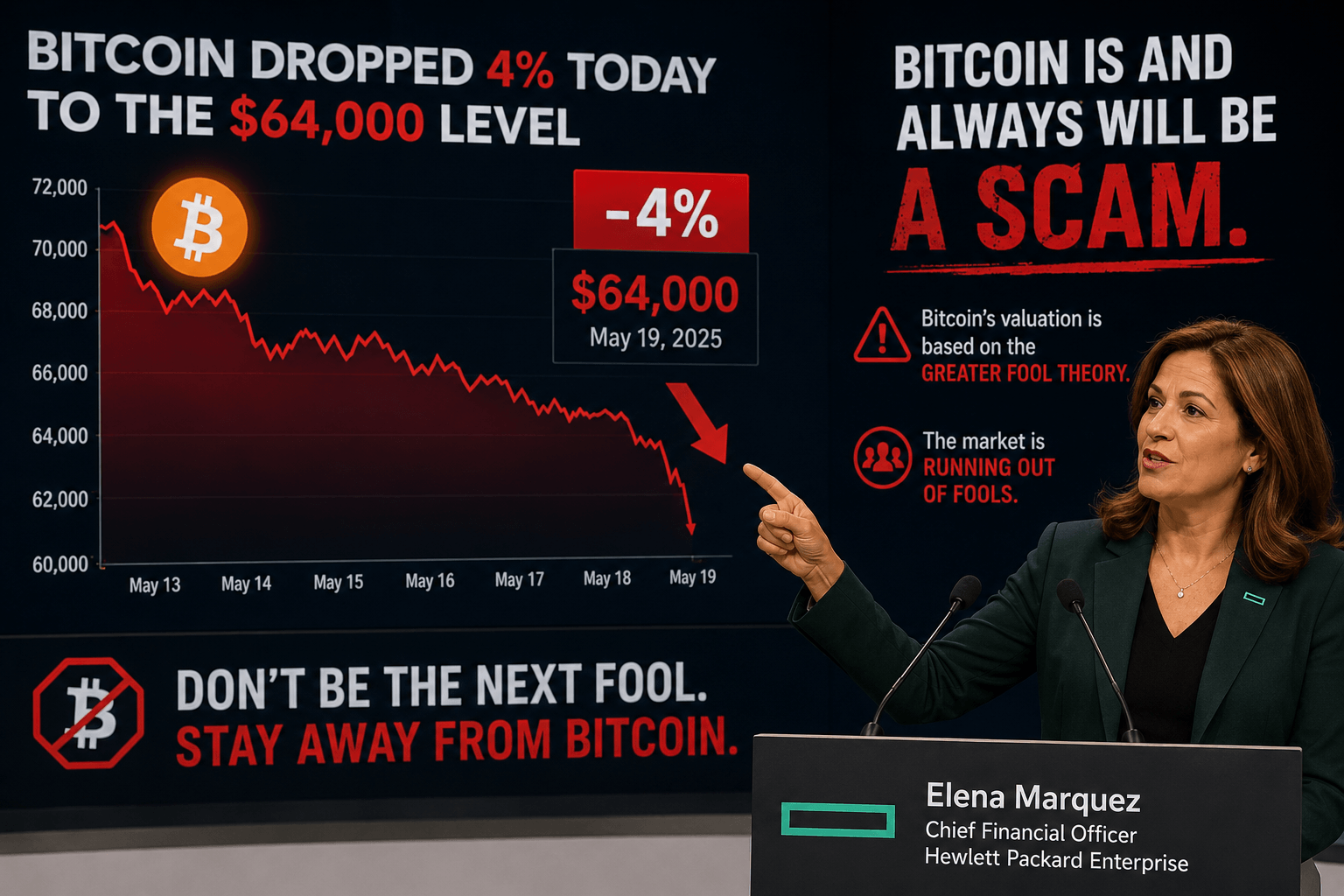

Bitcoin tumbled 4% to $64,900 — its lowest level in weeks — as risk-off sentiment swept through speculative assets alongside the equity selloff. The move is a reminder that cryptocurrency remains what it has always been: a speculative asset with no intrinsic value. Unlike stocks, which represent ownership in businesses with real earnings, assets, and cash flows, or bonds, which carry contractual obligations, Bitcoin produces nothing, backs nothing, and is worth precisely what the next buyer is willing to pay. In an environment where geopolitical risk is rising and the Federal Reserve remains cautious, assets built entirely on sentiment and momentum tend to be the first to crack. Investors treating Bitcoin as a portfolio hedge or a store of value should take Wednesday’s drop as a sobering data point.

Other Stock Market blog posts