| 📊 Alain’s Holdings — June 22, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 686.10 | -2.01 | -0.29% |

| QQQ | Invesco QQQ Trust | 737.95 | -2.67 | -0.36% |

| XIU.TO | iShares S&P/TSX 60 ETF | 51.84 | +0.11 | +0.21% |

A Market of Two Cities:

Chips Soar, Russell Hits 3,000

as Hyperscalers Collapse

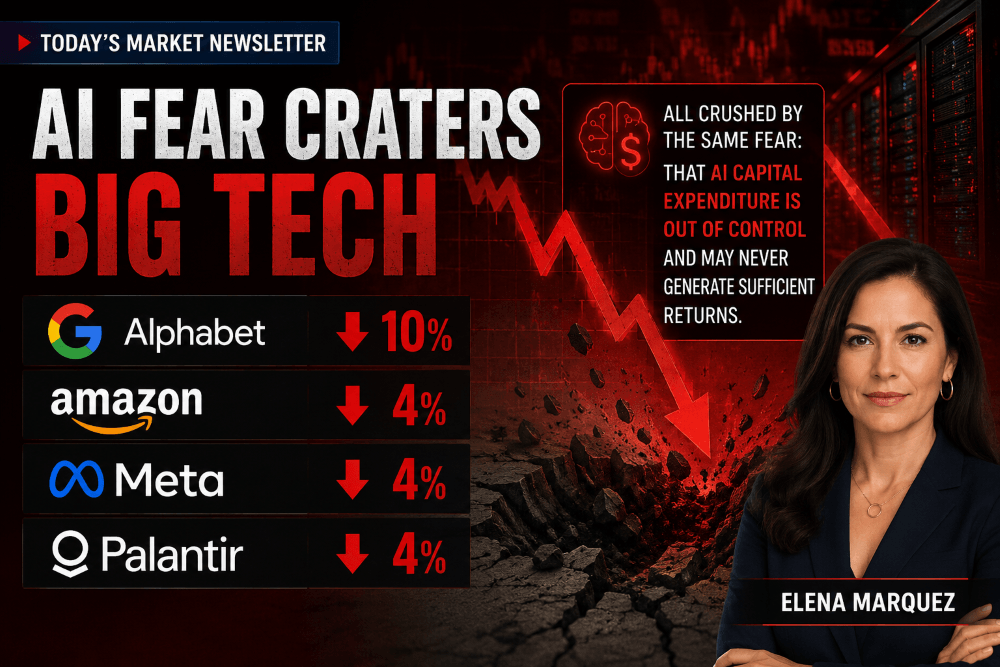

The most dramatic intra-market divergence of 2026. Micron and Sandisk each jumped 5% as the chip rally continued. The Russell 2000 crossed 3,000 for the first time in its history. But Alphabet cratered 10%, Amazon fell 4%, Meta fell 4%, and Palantir dropped 4% — all crushed by the same fear: that AI capital expenditure is out of control and may never generate sufficient returns. The Nasdaq-100 finished near flat as two opposite forces fought to a draw.

Index Close

Dow Jones

~51,637

Nasdaq Composite

~26,518

Nasdaq-100

Near flat / dn

Russell 2000

2,979–3,000+

Market Snapshot

The Day’s Great Divide

- Micron (MU) +5% — pre-earnings positioning; reports this week

- Sandisk (SNDK) +5% — storage/memory riding chip wave

- Nvidia (NVDA) +1.34% — led Dow gainers

- Caterpillar (CAT) +2.49% — industrials outperform

- Amgen (AMGN) +1.45% — healthcare steady

- Banks: BofA + JPMorgan +~2% — financials benefit from rate environment

- AbbVie (ABBV) +1% — agreed to acquire Apogee Therapeutics for $10.9B cash

- Astera Labs +5.42% — welcomed into Nasdaq-100

- Flex (FLEX) +5.57% — added to S&P 500

- Russell 2000 +2.12% — crossed 3,000 for first time ever

- Alphabet (GOOGL) −10% — largest single-day loss in weeks

- Amazon (AMZN) −4% — AI capex / Home Depot replaced it in Dow?

- Meta (META) −4% — AI spending concerns deepen

- Palantir (PLTR) −4% — high-multiple AI name sold off

- Oracle (ORCL) −2%+ — extended post-earnings capex concern

- SpaceX (SPCX) −5% — new bond offering announcement

- CoreWeave (CRWV) −5.58% — removed from Nasdaq-100

- Rocket Lab (RKLB) −6.44% — removed from Nasdaq-100

- Home Depot (HD) −1.88% — Dow laggard

⚠ The Week’s Dominant Theme

The AI Capex Reckoning: Are the Hyperscalers Spending Too Much?

🟢 The Bull Case

AI infrastructure spending is building a capability moat that will compound for years. Starlink, AWS, Azure, and Google Cloud will monetize this compute at higher margins than today’s prices suggest. Oracle’s $553B backlog is real demand, not speculation. Nvidia’s sustained revenue growth vindicates every dollar spent.

🔴 The Bear Case

Alphabet, Meta, Amazon, and Oracle collectively plan to spend hundreds of billions in 2026 alone on AI infrastructure with no clear timetable for proportional revenue returns. Free cash flow is collapsing industry-wide. Alphabet’s $80B equity raise — the largest ever — suggests even the most profitable company in history cannot internally fund its AI ambitions. At some point, investors demand returns, not promises.

Monday’s selloff in hyperscalers was triggered by renewed investor focus on this debate — amplified by reports that Alphabet’s AI spending plans are accelerating even beyond the $80B raise, and that Amazon and Meta face similar dynamics. The market is beginning to bifurcate between AI infrastructure enablers (chip manufacturers, memory companies, physical infrastructure) that have clear, current revenue from the buildout — and AI hyperscale spenders (the Googles, Metas, Amazons) whose returns remain a future promise against present-day massive cash consumption.

🔄 Quarterly Index Rebalance — Nasdaq-100 & S&P 500

✅ Added to Nasdaq-100

- Astera Labs (ALAB) +5.42%

- Teradyne (TER) +4.25%

❌ Removed from Nasdaq-100

- CoreWeave (CRWV) −5.58%

- Rocket Lab (RKLB) −6.44%

The quarterly rebalance created mechanical buying and selling pressure at the open. Additions surged as index funds were forced buyers; deletions were sold. In the S&P 500, Flex (+5.57%) was added and celebrated, while Marvell Technology (−0.78%) saw modest selling on its inclusion — an irony given it was one of the week’s biggest winners just a week earlier. These mechanical flows created some of the day’s most dramatic single-stock moves independent of any company-specific news.

Notable Movers

📈 Winners

📉 Losers

What Happened Today

The market is splitting in two — and Monday made it unmistakable. Semiconductor manufacturers and infrastructure enablers are rallying on genuine revenue from the AI buildout; AI hyperscalers and platform companies are selling off on the fear that their AI capital spending will not generate proportional returns. Both narratives are happening simultaneously in the same market, in the same session, pulling major indexes in opposite directions. The Nasdaq Composite rose 1.91% — but only because chips outweighed the hyperscaler damage. The Nasdaq-100 finished near flat as the two forces roughly cancelled out.

Alphabet’s 10% single-day collapse was the headline number. Reports that Alphabet’s AI spending plans are accelerating even beyond its historic $80 billion equity raise alarmed investors who are already questioning whether the AI buildout can generate sufficient returns. The same concern weighed on Amazon (−4%), Meta (−4%), Palantir (−4%), and Oracle (−2%+). These are companies that are collectively spending hundreds of billions annually on AI infrastructure — and Monday’s market sent a clear message: patience for promises without near-term returns is running thin.

The Russell 2000’s historic close above 3,000 was the day’s most quietly significant milestone. The small-cap index — which represents nearly 2,000 domestic U.S. companies largely insulated from the AI capex debate — closed just above 3,000 for the first time in its history, ascending from a 52-week low of 2,088. The move reflects the growing confidence that falling oil prices, a resilient labor market, and the Iran peace deal’s economic tailwinds will benefit Main Street companies regardless of what happens in the mega-cap AI arms race. It also reflects the rotation away from concentrated mega-cap tech that has been building since Warsh’s FOMC shock last Wednesday.

AbbVie agreed to acquire Apogee Therapeutics for approximately $10.9 billion in cash — the largest pharmaceutical deal of the week and a reminder that M&A activity outside the AI sector continues at a healthy pace. Apogee focuses on next-generation immunology drugs; the deal gives AbbVie a pipeline to offset the long-term revenue risk from Humira biosimilar competition.

🚀 SpaceX (SPCX) −5% — New Bond Offering Spooks Shareholders

SpaceX fell roughly 5% Monday after announcing a new bond offering — its second capital market transaction in just over a week following the $75 billion IPO. The market reacted with mild concern: a company that just raised $75 billion now needs additional debt financing, raising questions about the pace of capital consumption from the $60 billion Cursor acquisition and ongoing Starlink and Terafab expansion. SPCX remains approximately 40% above its $135 IPO price even after Monday’s decline — so this is not a crisis, but it is a reminder that the IPO pop does not eliminate the need for ongoing capital discipline.

₿ Bitcoin — ~$64,210 (+0.08%) · Essentially Unchanged · Holding Ground

Bitcoin was nearly flat on Monday, hovering around $64,210 — up just 0.08% on the day. After last week’s volatile swings (down on Warsh’s hawkishness, steady after the peace deal), Bitcoin appears to be consolidating around the $63,500–$64,500 range. The near-total absence of directional movement on a day when some individual equities moved 10%+ underscores Bitcoin’s sensitivity to broad macro catalysts rather than sector-specific stories. The AI capex debate that rocked Alphabet and Meta did not register as meaningful for Bitcoin — which makes sense, since Bitcoin has no earnings, no cash flows, and no connection to AI revenue cycles. It remains a pure macro-sentiment asset, and Monday’s macro was mixed enough to produce near-zero net movement.

What to Watch This Week

- Micron earnings (Tuesday after close): MU rose 5% Monday on pre-earnings enthusiasm. This is the week’s biggest chip-sector data point — a strong print on AI-driven memory demand would confirm the SOX all-time high was justified. A miss would test chip conviction after two weeks of volatility.

- FedEx earnings (Tuesday after close): A bellwether for global trade and logistics. With oil at $75 and declining, FedEx’s fuel cost tailwind may produce a meaningful margin beat. Watch for guidance on freight volumes as an economic health check.

- S&P Global Flash PMIs (Tuesday): The first read on June manufacturing and services activity — important context for whether the economy is absorbing the Warsh rate-hike signal or showing signs of stress.

- May PCE inflation (Thursday): The Federal Reserve’s preferred inflation measure. With WTI near $75 (down from $98 two weeks ago), May PCE could already show the early benefit of falling energy prices. A cool print would be the most powerful argument against the hawkish FOMC dot plot.

- Alphabet’s AI capex narrative: Monday’s 10% drop demands a response from Alphabet. Watch for any investor day commentary, analyst calls, or executive statements that attempt to frame the spending strategy in terms of return timelines — this is now the most important story in mega-cap tech.

Other Stock Market blog posts