| 📊 Alain’s Holdings — June 18, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 688.11 | +6.70 | +0.98% |

| QQQ | Invesco QQQ Trust | 740.62 | +18.11 | +2.51% |

| XIU.TO | iShares S&P/TSX 60 ETF | 51.73 | -0.22 | -0.42% |

Chips Stage a Historic Comeback.

Trump’s Apple–Intel Deal

Sends the SOX to a Record.

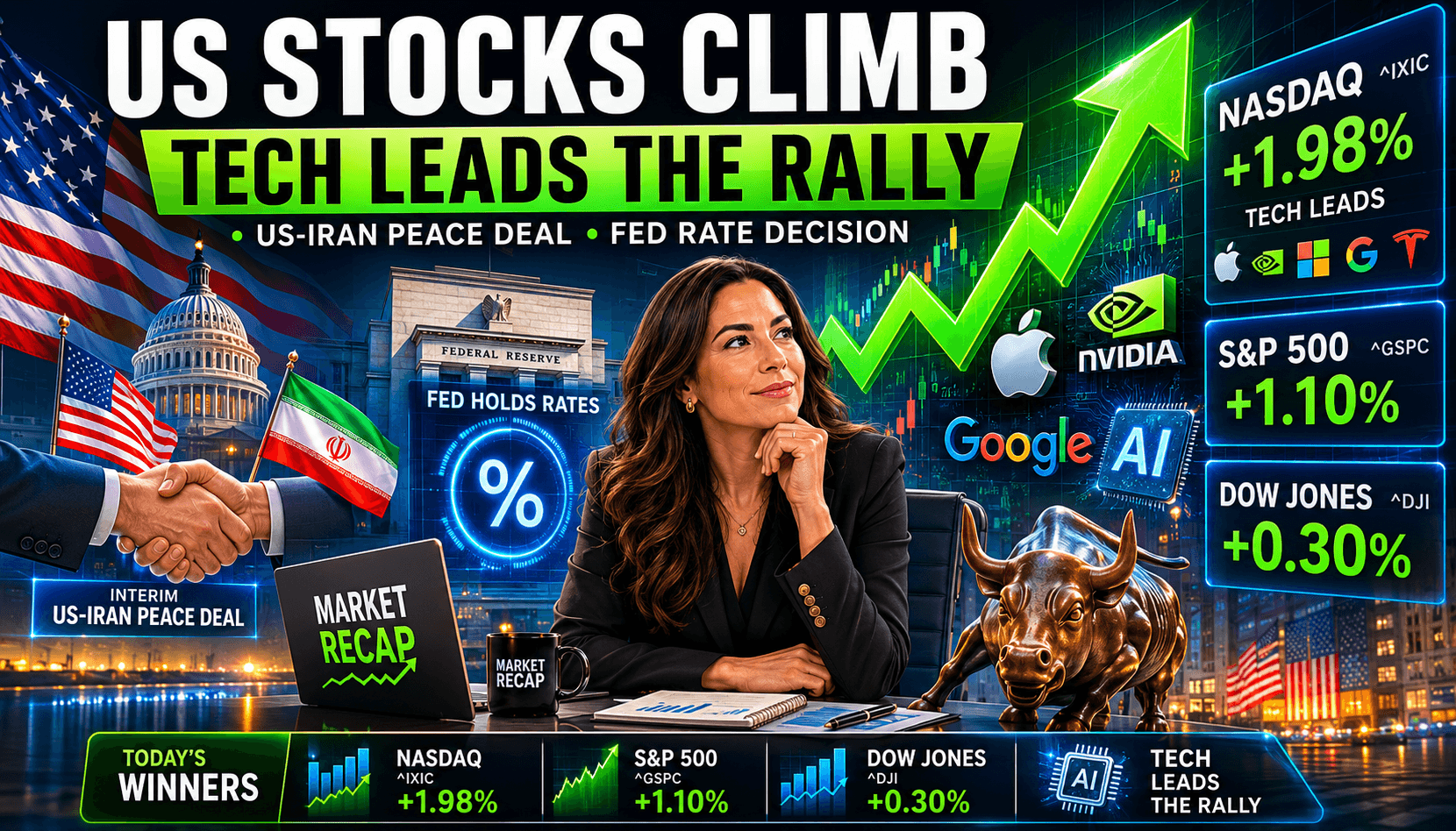

Twenty-four hours after Warsh’s hawkish FOMC shock rattled tech stocks, markets reconsidered. A Trump Truth Social post confirming Apple had agreed to work with Intel on U.S.-made chips ignited the semiconductor sector — the Philadelphia Semiconductor Index (SOX) surged more than 6% to an all-time high. The S&P 500 climbed 1%, the Nasdaq 100 advanced 2.3%, and Intel alone jumped more than 10%. Markets close Friday for Juneteenth.

Index Close

S&P 500

~7,476

Nasdaq 100

+2.3%

Dow Jones

~51,820

SOX (Chip Index)

Record High

Market Snapshot

🇺🇸 The Catalyst — Trump Confirms Apple–Intel Chip Partnership

“Apple Has Agreed to Work With Intel to Design and Build Its Chips in America”

In the early hours of Thursday, President Trump posted on Truth Social: “Apple has agreed to work with Intel to design and build its Chips in America.” The announcement — which neither Apple nor Intel had formally confirmed as of market close — sent Intel surging more than 9% in pre-market trading and confirmed what Bloomberg had previously reported: that Apple had been holding exploratory discussions about using Intel’s foundry services to produce main processors domestically.

Trump framed the deal as part of his broader semiconductor reshoring agenda: “Stupid Presidents took our Economy for granted, and let Taiwan and others steal our Semiconductor Factories… I decided to help Intel because we need to design and build our Chips right here in America. First, we helped bring in Nvidia, and they agreed to build their first level Chips with Intel.” Trump also highlighted Intel’s upcoming Terafab chipmaking facility linked to Elon Musk, where Nvidia’s first foundry orders are reportedly headed.

For Apple, the deal represents strategic supply chain diversification — reducing its concentration risk away from TSMC in Taiwan amid ongoing geopolitical tensions. For Intel, the Apple endorsement from the world’s most valuable company validates CEO Lip-Bu Tan’s foundry turnaround thesis. Intel’s 18A-P process entered risk production Wednesday; yield rates are reportedly running ahead of internal targets by two quarters. The stock, which traded near $19 a year ago, closed Thursday at a market cap approaching $609 billion — up 464% over 12 months.

“First, we helped bring in Nvidia, and they agreed to build their first level Chips with Intel. Now Apple has agreed to work with Intel to design and build its Chips in America. We are bringing it ALL BACK!” — President Trump, Truth Social, June 18, 2026

📈 Philadelphia Semiconductor Index (SOX) — New All-Time High

The Philadelphia Semiconductor Index surged more than 6% to an all-time high on Thursday — the same index that had crashed 8.6% intraday just nine days earlier when Iran shot down a U.S. helicopter. Nvidia topped the S&P 500 on a points basis. Micron jumped 8% — the company reports earnings next week and investors appear to be pre-positioning for a strong quarter. Broadcom advanced more than 4% alongside AMD, recovering sharply from the post-FOMC selloff. The SOX’s record close is a remarkable reversal from the sector’s extreme volatility over the past two weeks.

Notable Movers

📈 Winners

📉 Under Pressure

What Happened Today

Wednesday’s FOMC shock aged quickly. Less than 24 hours after Warsh’s hawkish dot plot sent the 2-year Treasury yield to 4.21% and the Nasdaq down 1.34%, markets opened Thursday with a completely different story: Trump’s Apple–Intel announcement, a recovering chip sector, and fresh evidence from oil markets that the Iran peace deal’s deflationary impact is accelerating. WTI crude fell another 3.28% to $73.52 — marking three consecutive sessions below $80 and the lowest level since early March. VIX fell 9.26% to 16.73, signaling that fear is fading as quickly as it arrived.

The semiconductor recovery was staggering in its speed. Nine days ago, the Philadelphia Semiconductor Index hit an intraday low of −8.6% on the Iran helicopter crisis. On Thursday, the SOX hit an all-time high, advancing more than 6% — a swing of roughly 15 percentage points in less than two weeks. This kind of volatility underscores how much of the chip sector’s moves have been driven by geopolitical and macro sentiment rather than fundamental changes in the AI buildout thesis. The underlying demand — evidenced by Oracle’s $553B backlog, Broadcom’s $29.4B quarterly guide, and Micron’s pre-earnings momentum — never went anywhere.

Markets also began reconsidering Warsh’s hawkish message. Several analysts flagged that buried in the FOMC statement was an important acknowledgment: Warsh noted Fed policy appears restrictive “vis-à-vis the housing market, but not financial markets.” Housing starts have collapsed to a 6-year low, the 30-year mortgage rate is at 6.52%, and consumer inflation expectations remain tied almost entirely to energy — which is now falling fast. Goldman Sachs Asset Management maintained its base case that the Fed can “just about avoid hikes” if oil stays low. With WTI at $73.52 — down from $98 just two weeks ago — the June CPI print (due mid-July) could give the Fed the cover it needs to hold indefinitely.

The Dow’s composition told its own story: IBM fell 5.43% on no specific news — likely some rotation out of the enterprise software name that had surged earlier in the week. Salesforce fell 2.73% and Chevron declined 2.16% as falling oil prices put energy revenues under pressure. But Caterpillar (+3.67%) and Home Depot (+2.83%) more than compensated, with both names benefiting from improving economic confidence and a potential infrastructure spending boost from the post-Iran reconstruction expectations.

🔄 Markets Reconsidering the Warsh Panic — Here’s Why

Wednesday’s selloff was real — but the post-FOMC reconsideration is equally real. Three factors are driving it: (1) Oil at $73.52 is directly deflationary — June CPI, due mid-July, could print well below May’s 4.2%, removing the primary justification for the nine hawkish dot-plot projections; (2) Warsh’s statement contained a dovish undercurrent — his comment that policy is “restrictive vis-à-vis the housing market” signals awareness of the domestic economic damage rising rates cause; and (3) The dot plot is projections, not commitments — Warsh himself said “I can’t give you guidance on what we’ll do next,” meaning the nine hike signals are contingent on data that is already turning favorable. Goldman’s Kay Haigh: “Our base case remains that the Fed can just about avoid hikes — but the path is narrow.”

📅 Markets Closed Tomorrow — Juneteenth (June 19)

U.S. equity markets are closed Friday, June 19, in observance of Juneteenth. The formal Iran peace deal signing ceremony is scheduled to take place in Switzerland on Friday, mediated by Pakistan, giving the week a historic geopolitical bookend on a market holiday. Futures markets and some international markets will remain open. Trading resumes Monday, June 22, with Micron Technology earnings and FedEx results among the first major catalysts of the new week — both reporting after next week’s close.

₿ Bitcoin — $63,857 (−2.09%) · Pulls Back as USD Holds Strength

Bitcoin fell 2.09% Thursday to $63,857, extending its retreat from Tuesday’s highs near $66,500. The pullback reflects the continued strength of the U.S. dollar — which surged 1% on Wednesday’s hawkish FOMC and held much of that gain Thursday — and some recalibration of the risk-on enthusiasm that followed the Iran deal. Bitcoin had tracked the Iran peace deal narrative closely on the way up last week; it is now tracking the rate-hike uncertainty narrative on the way down. This is precisely the pattern that defines Bitcoin as a speculative asset with no intrinsic value: it rises and falls with macro headlines because sentiment — and nothing else — determines its price. No earnings, no cash flows, no physical backing. When the dollar is strong and rate expectations are elevated, Bitcoin faces structural headwinds with no fundamental floor to arrest the decline.

What to Watch Next Week — June 22 Onwards

- Juneteenth signing ceremony (Friday, June 19): The formal U.S.–Iran peace deal signing in Switzerland takes place while U.S. markets are closed. Watch for any last-minute complications in published terms — particularly the 60-day nuclear negotiation window and the exact timeline of Iranian oil exports resuming.

- Micron Technology earnings (after close, week of June 22): MU was up 8% Thursday on pre-earnings positioning. Micron will be the first major semiconductor earnings report since Intel’s Apple deal confirmation and will serve as a key real-world check on AI-driven memory demand. Consensus expects strong results.

- FedEx earnings (same week): FedEx is a bellwether for global trade volumes, shipping costs, and consumer activity. With oil at $73.52, FedEx’s fuel costs have fallen sharply — watch for a margin beat.

- PCE inflation (end of June): The Fed’s preferred inflation gauge — Personal Consumption Expenditures — for May will be released late June. This is the data point that could definitively tell the Fed (and markets) whether the May CPI/PPI spike was a one-time energy shock or something more persistent.

- SOX record durability: The semiconductor index hit an all-time high Thursday. Whether it holds next week — or whether the Warsh rate-hike concern reasserts itself — will be the clearest signal of whether the AI chip trade has truly recovered from its two-week rollercoaster.