| 📊 Alain’s Holdings — June 17, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 681.41 | -8.34 | -1.21% |

| QQQ | Invesco QQQ Trust | 722.51 | -7.35 | -1.01% |

| XIU.TO | iShares S&P/TSX 60 ETF | 51.95 | -0.32 | -0.61% |

Warsh’s Hawkish Debut

Sends Stocks Tumbling

and Yields Surging

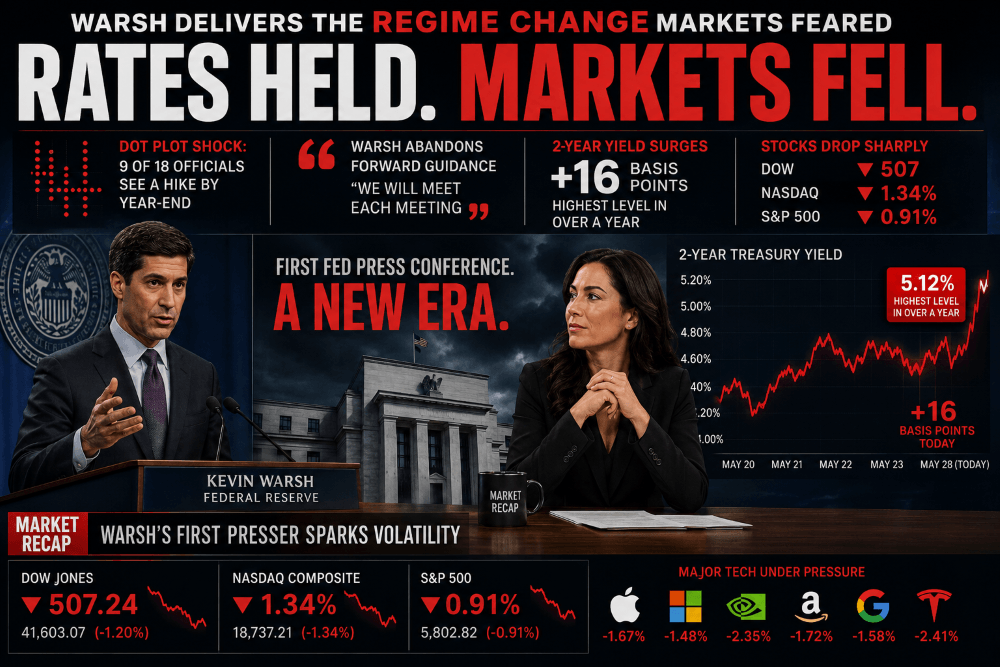

Kevin Warsh’s first Federal Reserve press conference delivered the regime change markets feared. Rates held, as expected — but the dot plot showed nine of 18 officials signaling a rate hike by year-end, Warsh publicly abandoned forward guidance, and the 2-year Treasury yield exploded 16 basis points to its highest level in over a year. Stocks fell sharply. The Dow dropped 507 points, the Nasdaq shed 1.34%, and major tech bellwethers bore the brunt.

Index Close

Dow Jones

51,492.55

S&P 500

7,420.10

Nasdaq Composite

26,021.66

2-Yr Treasury Yield

4.21%

Market Snapshot

🏦 FOMC Decision — Warsh’s First as Fed Chair

“We’ve Dropped Forward Guidance. I Can’t Tell You What We’re Going to Do Next.”

The Federal Open Market Committee voted unanimously to hold the federal funds rate at 3.50%–3.75%, unchanged since December 2025. The decision itself was fully expected — but nearly everything else about the meeting was a hawkish shock. The new dot plot showed nine of 18 FOMC members projecting at least one rate hike before year-end (of those nine, six favored multiple hikes). The median 2026 year-end forecast rose to 3.8% — up from 3.4% in March, and a quarter-point above the current rate. Markets fully priced in one 25-basis-point hike by December. The odds of a hike by October crossed 50%.

Warsh’s statement was notably short — a significant departure from prior Fed practice. It acknowledged that inflation “remains elevated relative to the Committee’s 2% goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy.” The statement removed the prior easing bias entirely. Warsh announced five task forces to overhaul Fed communications, the balance sheet, and other operations — signaling a structural regime change, not just a policy pivot.

Warsh also notably declined to submit his own rate forecast — the only FOMC participant to sit out the dot plot. He framed this as consistent with his view that the Fed chair should not be trying to “pre-commit” to a path when incoming data is uncertain. He wants markets to react to data, not to Fed guidance — a fundamental shift from the Bernanke-Yellen-Powell era of transparency.

“Economic activity is expanding at a solid pace despite elevated uncertainty… Productivity growth and capital investment are strong. The commitment to deliver [2% inflation] is strong, unanimous, and unambiguous — and that’s an important message we’ve missed for five years.” — Chair Kevin Warsh, June 17, 2026

🔴 The Dot Plot — What 9 of 18 Officials Are Signaling

The dot plot’s hawkish tilt reflects the cumulative effect of May CPI at 4.2%, PPI at 6.5%, and the May NFP blowout of 172,000 jobs. The Iran deal and falling oil prices should provide some relief in coming months — but Goldman Sachs Asset Management’s Kay Haigh noted: “Despite the recent pullback in oil, half of the members of the FOMC expect rate hikes as soon as this year, reflecting strong labor market and inflation data. Our base case remains that the Fed can just about avoid hikes, but the path is narrow.” Markets are no longer giving the Fed the benefit of the doubt — a December hike is now fully priced in per Bloomberg data.

Bond Market Reaction

Notable Movers

📉 Losers — Tech Led Down

📈 Bucking the Trend

What Happened Today

Markets entered the session cautiously optimistic and left rattled. The Dow actually hit a fresh intraday all-time high — its third consecutive session reaching new records — in the morning session before the 2 PM FOMC announcement. The statement, once it arrived, confirmed the rate hold but stripped out the easing bias entirely and laid the hawkish groundwork. Stocks dipped immediately. Then Warsh took the podium, and the session took a decisive turn for the worse.

The dot plot was the knockout punch. Half of the 18 FOMC participants who submitted projections see at least one rate hike by year-end — an extraordinary signal from a committee that had been projecting one cut just three months ago in March. The median year-end fed funds forecast moved to 3.8% — 25 basis points above the current target. Traders immediately repriced: Bloomberg data showed a December hike fully priced in, and odds of an October hike crossing 50%. The 2-year Treasury yield, most sensitive to near-term rate expectations, exploded 16 basis points to 4.21% — its highest level in over a year.

Warsh’s communication style itself was a market event. In abandoning forward guidance — openly declaring “I can’t give you any guidance on what we’re going to do next” — he is making a clean break from the Bernanke-Yellen-Powell era of highly telegraphed policy. For markets that have spent a decade pricing in Fed forward guidance, this is structurally destabilizing. Wolfe Research analyst Tobin Marcus had anticipated this shift, writing ahead of the meeting that Warsh would use his first meeting to signal “regime change” rather than make concrete policy moves. That forecast proved accurate. Warsh also announced five task forces to review Fed communications, the balance sheet, and economic data methodology — changes that could take months to play out but signal a fundamental rethinking of how the central bank operates.

The sell-off was concentrated in rate-sensitive tech. Microsoft, Meta, Alphabet, and Amazon all closed in the red, dragging the Nasdaq to a 1.34% loss. The higher-for-longer rate environment compresses the present value of future cash flows — precisely the valuation mechanism that drives high-multiple AI and tech names. The dollar index surged roughly 1% — its best single day in nearly a year — as rate-hike expectations repriced globally. Gold, which had rallied on the Iran peace deal earlier in the week, fell more than 2% as the stronger dollar and higher real yields removed the safe-haven premium.

The one piece of genuinely good news: WTI crude oil fell 2.6% to $78.66 — below $80 for the first time since early March. The Iran deal’s impact on oil is real and accelerating. If this disinflationary impulse shows up in June CPI data (due in mid-July), the Fed will have the cover it needs to stay on hold rather than hike. Goldman Sachs Asset Management’s base case remains that the Fed “can just about avoid hikes — but the path is narrow.”

🛢️ The Silver Lining — WTI Below $80 for the First Time Since March

Even on a hawkish Fed day, oil’s collapse remains the most important macro variable for markets. WTI fell 2.6% to $78.66 — well below last week’s peak of ~$98. If oil sustains this level or falls further, June CPI (released mid-July) will likely show a dramatic reversal from May’s 4.2% reading. A June CPI print in the 2.5–3.0% range would make rate hikes politically and mathematically difficult to justify — even for Warsh’s newly hawkish committee. The Iran deal’s deflationary impact may ultimately save markets from the rate hikes the dot plot is now threatening.

₿ Bitcoin — Retreating on Rate-Hike Signal, Falling Back From Recent Highs

Bitcoin fell on Wednesday as the hawkish FOMC reaction sent the U.S. dollar surging and rate expectations spiking — both classically negative inputs for speculative risk assets. After recovering from last week’s low of $60,783 to highs near $66,500 on Tuesday, the rate-hike signal is a reminder that Bitcoin’s recovery was entirely macro-sentiment-driven. A genuine rate hike would represent a significant headwind: higher real rates increase the opportunity cost of holding non-yielding assets, and Bitcoin — which produces no earnings, holds no physical backing, and generates no cash flows — has no fundamental anchor to cushion the impact. Wednesday’s selloff is Bitcoin doing exactly what it always does: reacting to the macro environment rather than any change in its own underlying value, because there is none.

What to Watch the Rest of This Week

- Treasury yields (Thursday/Friday): The 2-year’s 16-basis-point jump to 4.21% is the most important market signal of the week. Watch whether it holds or reverses as investors digest Warsh’s words more carefully — particularly his acknowledgment that “Fed policy appears to be restrictive vis-à-vis the housing market, but not financial markets,” which some interpreted as a relatively dovish undercurrent beneath the hawkish headline.

- Housing starts already collapsing: Tuesday’s data showed U.S. housing starts fell 15.4% in May to 1.177 million — the lowest since May 2020. Higher mortgage rates (30-year at 6.52%) are already biting. If the Fed hikes further, the housing market contraction deepens sharply.

- Oil — can WTI hold below $80? Wednesday’s $78.66 is a critical level. A sustained move toward $75 would begin to show up in inflation expectations models and could prompt Fed officials to walk back the hawkish dot plot language in upcoming speeches.

- Friday, June 19 — Juneteenth (markets closed): The formal Iran peace deal signing ceremony in Switzerland takes place on a day when U.S. markets are closed. Watch for any last-minute complications in the published terms — particularly the 60-day nuclear negotiation window.

- SpaceX (SPCX): After hitting an all-time high of $225.64 on Tuesday and pulling back alongside the broader market Wednesday, watch whether SPCX can hold above $200 as rate-hike fears weigh on high-multiple growth names.

Other Stock Market blog posts

- Future of the Auto Industry: Why BMW’s Problems Are Just the Beginning

- Stock Market Recep, Tuesday, June 16, 2026

- Adobe Loses Customer Love: The Stock Is Crashing