Quick-Service Restaurants vs the S&P 500

The Quick-Service Restaurants sector is quietly falling behind the broader market. While the S&P 500 has delivered roughly +30% over the past 12 months, most major QSR (Quick-Service Restaurants) stocks have failed to keep pace.

This divergence is not random. It reflects deeper structural pressures affecting consumer behavior, pricing power, and competition within the sector.

Performance Snapshot: Winners and Losers

Here’s how key Quick-Service Restaurants stocks have performed over the past year:

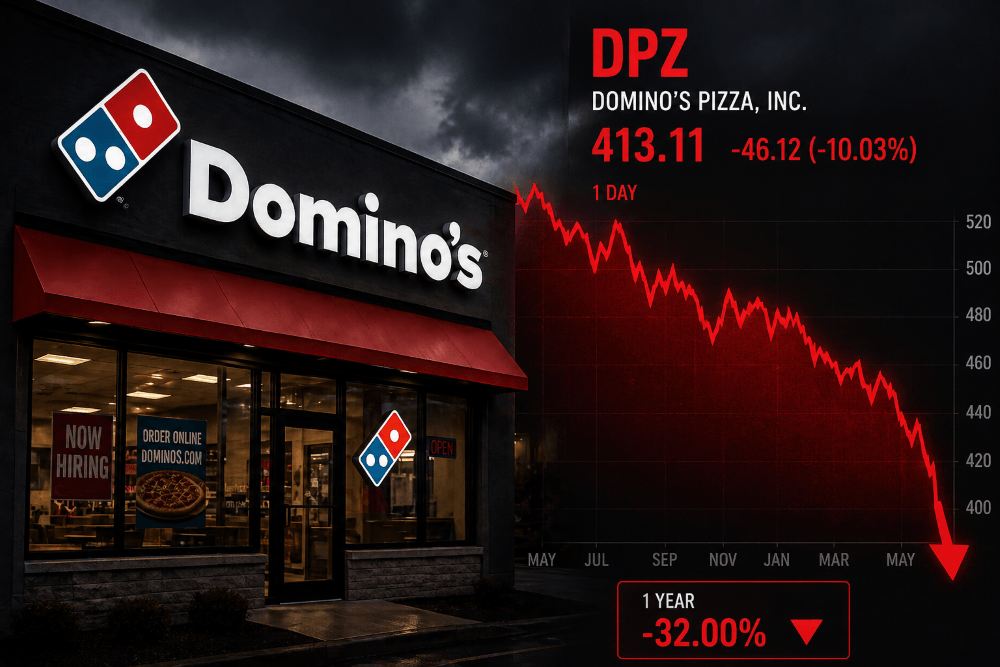

- Domino’s, DPZ: -32%

- Including a sharp ~10% drop following disappointing earnings

- Yum! Brands YUM: +6%

- Papa John’s. PZZA: +10%

- Restaurant Brands, owner of Burger King, QSR: +27%

- McDonals, MCD: -7%

At first glance, the sector looks mixed. But relative to a +30% benchmark, the picture is clear: this is broad underperformance.

Why Quick-Service Restaurants Are Underperforming

1. The consumer is weakening

Quick-Service Restaurants depend heavily on discretionary spending.

When consumers feel pressure from inflation, interest rates, or energy costs, they cut back on takeout and delivery first.

Even value-oriented brands like Domino’s Pizza are seeing softer demand.

2. Price competition is intensifying

The QSR model relies on volume. When traffic slows, companies respond with promotions.

This leads to:

- Margin compression

- Lower profitability

- Reduced investor confidence

Pizza chains are especially vulnerable due to constant discounting.

3. The pizza segment is structurally weaker

Within Quick-Service Restaurants, pizza chains have been hit hardest.

- Domino’s Pizza (DPZ) down sharply

- Papa John’s International (PZZA) struggling to grow

- Pizza Hut under Yum! Brands facing store challenges

The common traits:

- Heavy reliance on delivery

- High promotional intensity

- Limited differentiation

4. Diversification is saving some players

Not all QSR companies are equally exposed.

- Restaurant Brands International (QSR) benefits from multiple brands

- McDonald’s (MCD) has global scale and strong pricing power

This explains why QSR (+27%) is much closer to the S&P 500 than DPZ.

The Key Trend: Fragmentation Within the Sector

The most important takeaway is not just underperformance. It’s divergence.

We are seeing a split between:

1. Pure-play, category-focused chains

- Domino’s (DPZ)

- Papa John’s (PZZA)

→ More volatile, more exposed to consumer weakness

2. Diversified global operators

- Yum! Brands (YUM)

- Restaurant Brands (QSR)

- McDonald’s (MCD)

→ More resilient, better positioned to absorb shocks

What Investors Should Take From This

1. This is not a one-stock problem

Domino’s decline is not an isolated event.

It reflects broader pressures across Quick-Service Restaurants, especially in the pizza segment.

2. Relative performance matters more than absolute returns

A stock rising +10% may look strong.

But if the S&P 500 is up +30%, that’s significant underperformance.

3. Business model matters more than brand strength

In this environment:

- Scale beats specialization

- Diversification beats focus

- Pricing power beats promotions

4. The sector may be entering a cyclical downturn

Quick-Service Restaurants tend to perform well in stable or mildly weak economies.

But when consumer stress rises sharply, even value players get hit.

Final Thought

The Quick-Service Restaurants sector is not collapsing. But it is clearly lagging.

Investors should view this as a rotation signal, not a panic signal.

Capital is flowing toward stronger, more diversified businesses, and away from narrowly focused, price-sensitive models.

Personally, if I had any Dominos I would get out of that trade as soon as possible.

It’s time to get out of Dominos

For investors holding DPZ, the recent earnings miss and sharp price decline should be taken seriously, not dismissed as short-term noise. The stock is not only down significantly, but it is also underperforming both its peers and the broader S&P 500, suggesting a deeper shift in momentum. With weakening consumer demand, heavy reliance on promotions, and increasing competition in the pizza segment, the risk-reward profile has deteriorated. Unless an investor has a strong long-term conviction in a turnaround, this may be a prudent moment to step aside and reallocate capital toward stronger, more resilient names within the Quick-Service Restaurant space.

FAQ: Quick-Service Restaurants Stocks

Why are Quick-Service Restaurants underperforming the S&P 500?

Because of weaker consumer spending, increased competition, and margin pressure from heavy discounting.

Which QSR stocks are performing best?

QSR and YUM are holding up better due to diversification.

Why is Domino’s stock down so much?

DPZ declined due to disappointing earnings, weak same-store sales, and heavy reliance on promotions.

Is this a good time to invest in QSR stocks?

It depends on the company. Diversified operators may offer resilience, while pure-play pizza chains remain more exposed to economic pressure.

Previous stock market posts