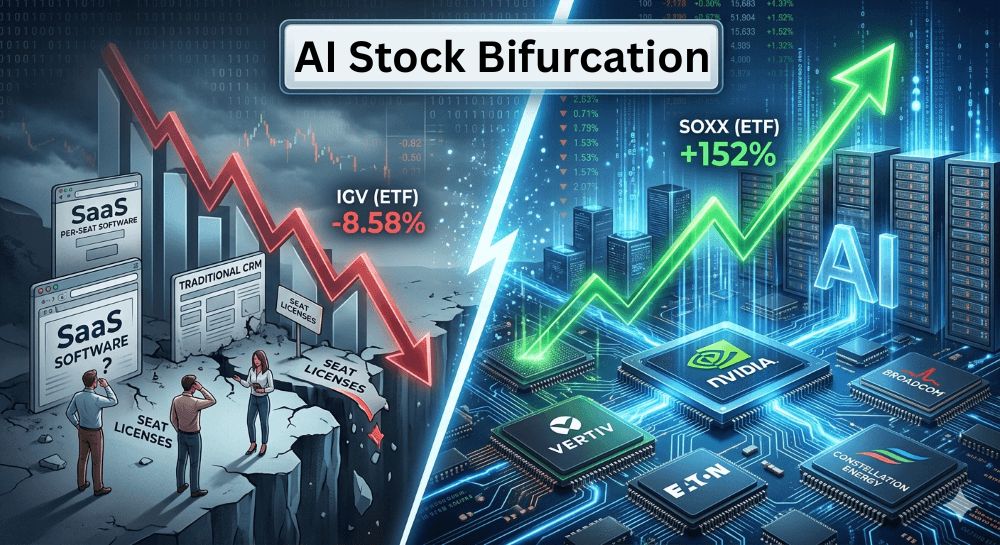

The technology sector is currently experiencing a historic AI stock bifurcation. While semiconductor giants are reaching all-time highs, many established software companies are struggling to maintain their valuations.

This “inner fight” in tech has created a massive performance gap. For example, the iShares Semiconductor ETF (SOXX) has skyrocketed by over 150% in the last year, while the iShares Expanded Tech-Software Sector ETF (IGV) has decline 8% over the same time period.

As an investor, understanding why this split is happening is crucial for protecting your portfolio. We are witnessing a transfer of value from the application layer to the infrastructure layer.

The Rise of Infrastructure: Why Hardware is King

Currently, the market is in the “Build” phase of the AI revolution. Companies are racing to build the data centers required to train Large Language Models (LLMs).

This has created a massive tailwind for companies that provide the “physicality” of AI. These are the “picks and shovels” of the modern gold rush.

- Nvidia (NVDA): The undisputed leader in AI training chips.

- Broadcom (AVGO): A dominant force in networking and custom AI silicon.

- Vertiv Holdings (VRT): A crucial provider of cooling and power systems for data centers.

The Software Struggle: The Fear of “Seat Compression”

The AI stock bifurcation is most painful for traditional Software-as-a-Service (SaaS) providers. The primary reason is a phenomenon known as “seat compression.”

The sharp decline in software stocks is called the SaaSpocalypse and we can blame it all on Calude.ai which is powerful enough to do the work that many of those software companies were doing for a small fraction of the cost.

Historically, software companies sold licenses per human user. However, as AI agents become more capable, companies may need fewer human employees to perform the same tasks. If an AI agent can do the work of five people, the software provider loses four paid “seats.”

The companies affected most fall into three categories: horizontal point solutions, “per-seat” model giants, and UI-heavy applications.

1. Most Impacted Public Companies (2026 Performance)

The following heavyweights have seen significant year-to-date (YTD) declines as of early 2026 due to fears of AI disintermediation:

| Company | Recent Performance (YTD 2026) | Primary Vulnerability |

| Atlassian (TEAM) | -57% | High exposure to developer-centric workflows that AI is now automating. |

| Workday (WDAY) | -43% | Slowing growth in HR/Finance and a legacy per-seat model under pressure. |

| Adobe (ADBE) | -30% | Fears that AI generation tools will reduce the need for specialized design software. |

| Salesforce (CRM) | -30% | Market saturation and the rising capability of AI “agents” to handle CRM tasks autonomously. |

2. Why These Companies are Struggling

The crisis isn’t just about stock prices; it’s a fundamental challenge to how these companies make money.

- The “Death of the Seat”: Traditional SaaS revenue is tied to the number of human users (seats). As AI agents like Claude Cowork or OpenAI Frontier handle the work of multiple people, enterprises are demanding consumption-based or outcome-based pricing rather than paying for idle software seats.

- Vibe Coding & Low Barriers: New AI tools allow startups to replicate complex software features (“vibe coding”) much faster than before, eroding the “moats” that protected billion-dollar companies.

- Budget Cannibalization: Enterprises are not increasing total IT spend; they are shifting funds away from “incremental” software updates to pay for expensive AI compute and specialized AI agents.

3. The “Safe” Exceptions

While the sector is in turmoil, analysts (including those from JP Morgan and HSBC) suggest that “mission-critical” infrastructure is more resilient. Companies like ServiceNow (NOW), Microsoft (MSFT), and CrowdStrike (CRWD) have fared better because their software acts as the “operating system” for the enterprise, making them harder to replace with standalone AI agents.

Summary of the “SaaSpocalypse” Narrative

“If AI agents can replicate what enterprise software does, then enterprise software is finished.”

This narrative drove the S&P Software & Services Index down over 20% in early 2026. While some view this as an overreaction, the shift toward Vertical SaaS (industry-specific tools for healthcare or manufacturing) and AI-native architectures is now a requirement for survival in the public markets.

The Winners of the Software Pivot

Not all software is doomed. The winners will be those who control the “System of Record” or successfully pivot to outcome-based pricing. It’s important to distinguish between companies that provide disposable tools (vulnerable) and those that provide essential infrastructure (resilient).

Here are the software sectors and specific companies currently showing strength:

1. The “Orchestrators” (AI-Native Infrastructure)

These companies don’t just sell a “seat” for a human to sit in; they provide the brain that runs the enterprise.

- Palantir (PLR): While it felt the initial market tremors, Palantir is emerging as a winner. In early 2026, it projected 61% growth, positioning itself as the “operating system” for AI. Unlike traditional SaaS, Palantir thrives on complexity—integrating AI into massive, messy datasets that standalone agents can’t handle.

- ServiceNow (NOW): Despite a 30%+ price drop in early 2026, it is being touted as a “value opportunity.” By acquiring Moveworks and launching Autonomous Workforce, they’ve pivoted to selling “AI agents” that resolve 90% of IT issues, effectively shifting their model to capture the value AI creates rather than just charging for human logins.

2. The Cybersecurity “Moat”

Security is non-negotiable, and the rise of AI agents has actually increased the “threat surface” for companies.

- CrowdStrike (CRWD): Recognized as a core “safe” play. They have integrated AI into their Falcon platform to secure the very AI infrastructure everyone else is rushing to build.

3. Vertical SaaS & High-Complexity Platforms

Software that is deeply embedded in a specific industry’s regulatory or physical workflow is much harder to replace.

- Shopify (SHOP): Standing out with a 26% gain recently. Because Shopify controls the physical flow of commerce—payments, shipping, and inventory—it isn’t as easily “disintermediated” by a coding agent as a simple marketing or HR tool might be.

- Datadog (DDOG): As companies deploy more AI models, they need more monitoring to ensure those models aren’t “hallucinating” or breaking. Datadog’s observability tools are seeing a 30%+ gain as they become essential for the AI era.

Summary: What Makes a “Winner” in 2026?

| Feature | Resilient Companies | Vulnerable Companies |

| Pricing Model | Consumption/Outcome-based | Per-user (Per-seat) |

| Function | Mission-critical / Infrastructure | UI-heavy / Point solution |

| Data Advantage | Proprietary workflow data | Public/Generic data |

| AI Integration | Agentic (AI does the work) | Copilot (AI helps a human) |

The Bottom Line: The companies doing well are those that have stopped fighting the AI agents and have instead started becoming the platform that manages them.

The Next Layer: Where to Focus Now

If you feel you missed the initial semiconductor surge, you can take a look at the Secondary Infrastructure layer—often called the “Physical Layer”—is arguably where the most durable value is being built right now.

While chips get faster every 12 months, the power grids, cooling loops, and transformers being installed today are 20-to-30-year assets. The “Secondary” layer extends into three specific sub-sectors:

1. The “Power Hungry” Layer (Electrical Equipment)

As GPU density increases, the electrical bottleneck isn’t just the chip; it’s the ability to get high-voltage power to the rack without melting the wires.

- Eaton (ETN): They are the “blue chip” of this layer. They manufacture the switchgear and power quality hardware that prevents AI data centers from blowing out the local grid. They recently committed over $30 million to a new Nebraska facility just to keep up with data center demand.

- Schneider Electric (SBGSY): A global leader in data center energy management. Their EcoStruxure platform is the standard for managing the complex power architectures required for liquid-cooled AI clusters.

- Powell Industries (POWL): A “hidden gem” in this space. They specialize in custom-engineered switchgear. They recently reported record earnings and announced a 3-for-1 stock split due to the surge in massive-scale industrial power orders.

2. The “Nuclear & Grid” Layer (Utilities)

Hyperscalers (Amazon, Google, Microsoft) are now the world’s largest buyers of clean energy. They need “always-on” power that solar and wind can’t provide alone.

- Vistra Corp (VST) & Constellation Energy (CEG): These are the primary owners of the U.S. nuclear fleet. They have signed massive, long-term power purchase agreements (PPAs) directly with hyperscalers. Vistra is currently seen as a high-conviction “power-as-a-service” play.

- GE Vernova (GEV): Since spinning off from GE, they have become a pure play on the electrification of the world. They make the gas turbines and grid orchestration software that utilities use to balance the sudden, massive loads from AI campuses.

3. The “Cooling & Enclosure” Specialists

Air cooling is dead for AI. Liquid cooling is now the industry standard for racks exceeding 50kW.

- nVent Electric (NVT): While Vertiv handles the overall system, nVent specializes in the “liquid-to-chip” manifolds and high-tech enclosures. They recently raised their three-year organic sales growth targets specifically because of the data center supercycle.

- Modine (MOD): Originally an automotive cooling company, they have pivoted hard into data center liquid cooling. They are often viewed as a smaller, more specialized alternative to the larger players.

Summary Comparison for the Secondary Layer

| Category | Leading Play | Market Role | 2026 Sentiment |

| Grid Power | Eaton (ETN) | High-voltage hardware | High (Heavy backlog) |

| Baseload | Vistra (VST) | Nuclear/Gas generation | High (Scarcity of power) |

| Cooling | nVent (NVT) | Rack-level liquid cooling | Rising (Niche leader) |

| Connectivity | Belden (BDC) | Fiber & cabling | Stable |

Frequently Asked Questions

1. Why is software falling while chips are rising? Investors are prioritizing hardware because it is a tangible requirement for AI. Software faces uncertainty due to “seat compression” where AI replaces human users who previously paid for licenses.

2. Is it too late to buy semiconductor stocks? While valuations are high, the transition to the “Inference Era” suggests long-term demand remains strong. However, focus on companies providing cooling and power (the infrastructure) rather than just the chips.

3. Which software stocks are safe? Software companies with a deep “data moat” or those that own the “System of Record” are safer. Look for companies moving toward usage-based or outcome-based pricing models.

Previous stock market posts