Norwegian Cruise Earnings Signal Trouble for the Sector

The latest Norwegian Cruise earnings report has sent a clear message to investors: even in a strong demand environment, profitability remains fragile.

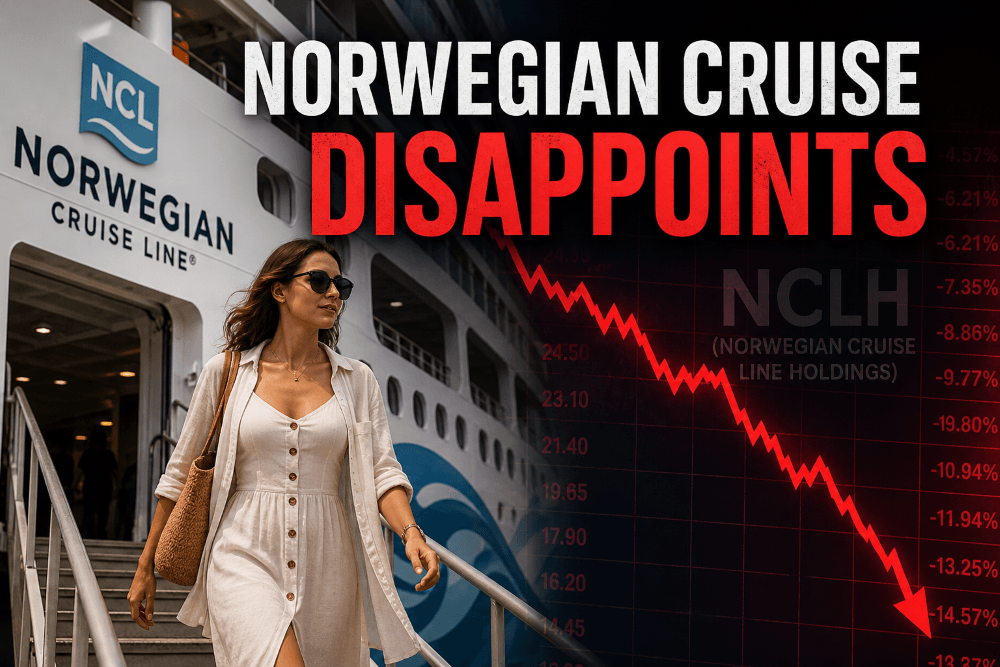

Norwegian Cruise Line Holdings cut its 2026 outlook, citing rising fuel costs and softer demand tied to geopolitical tensions. The stock dropped sharply, underperforming the broader consumer cyclical sector. Norwegian (NCLH) is down 0.46% for the past 12 months while the Consumer Discretionary Sector (XLY) is up 17% over the same time period.

This isn’t just a one-company issue. It’s a warning shot for the entire cruise industry.

A Strong Industry… With Weak Margins

At first glance, the cruise sector looks healthy.

Demand remains robust:

- Record passenger volumes

- Strong forward bookings

- High customer loyalty

Cruises are increasingly viewed as “value vacations,” bundling lodging, food, and entertainment into one price.

But here’s the problem:

Revenue is strong. Profits are not.

Why margins are under pressure:

- Rising fuel costs (highly volatile)

- Geopolitical disruptions affecting routes

- Elevated debt levels from the pandemic era

- Inflation in labor and operations

This creates a paradox: full ships, but squeezed earnings.

How Norwegian Compares to Its Competitors

Not all cruise companies are created equal. Norwegian’s disappointing performance highlights key differences in the sector.

1. Norwegian Cruise Line Holdings (NCLH)

- Mid-sized operator

- Higher debt burden

- Lower margins than peers

- Recent execution missteps

Norwegian sits in an uncomfortable middle position: not as premium as top-tier competitors, but without the scale advantages of larger players. Norwegian (NCLH) is down 0.46% for the past 12 months.

👉 Outlook: Likely to lag in stock performance

2. Royal Caribbean Group (RCL)

- Premium positioning

- Industry-leading margins

- Strong pricing power

- Consistent execution

Royal Caribbean has emerged as the best operator in the space. Its ability to command higher prices and maintain efficiency gives it a significant edge.

👉 Outlook: Most likely to outperform. Royal Caribbean Group (RCL) is up 13% for the past 12 months.

3. Carnival Corporation (CCL)

- Largest operator globally

- Mass-market focus

- Significant debt, but strong scale advantages

Carnival benefits from size, but its lower-end positioning limits pricing power.

👉 Outlook: Middle-of-the-pack performance. Carnival Corporation (CCL) is up 31% for the past 12 months.

Key Challenges Facing the Cruise Sector

Investors should not ignore the structural risks.

1. Fuel Price Volatility

Fuel is one of the largest costs for cruise operators.

A spike in oil prices can quickly erase profits, as seen in the latest Norwegian Cruise earnings report.

2. High Debt Levels

Cruise companies took on massive debt during the pandemic.

While revenues have recovered, balance sheets remain stretched.

3. Geopolitical Risks

Tensions in regions like the Middle East can:

- Increase fuel costs

- Disrupt itineraries

- Impact consumer confidence

4. Sensitivity to Economic Cycles

Cruises are discretionary spending.

If consumer sentiment weakens, demand could quickly follow.

Opportunities in the Cruise Industry

Despite the risks, the sector still offers long-term upside.

1. Strong Demand Tailwinds

- Aging population with time and money to travel

- Growth of middle-class travelers globally

- Increasing popularity of experiential travel

2. Pricing Power (Selective)

Premium operators can maintain pricing strength even in uncertain environments.

3. Operating Leverage

If fuel costs stabilize, profits could rebound sharply.

This makes cruise stocks highly sensitive to macro improvements.

Investment Outlook: Proceed With Caution

The takeaway from the latest Norwegian Cruise earnings is not that the industry is broken.

It’s that the sector is highly sensitive to external factors.

What investors should consider:

- Favor higher-quality operators (Royal Caribbean)

- Be cautious with highly leveraged players (Norwegian)

- Expect volatility driven by oil prices and geopolitics

This is not a smooth sailing sector—it’s a high-beta bet on travel demand and macro stability.

FAQ: Norwegian Cruise Earnings and Sector Outlook

1. Why did Norwegian Cruise earnings disappoint?

Norwegian lowered its outlook due to rising fuel costs and weaker demand in certain regions, which compressed profit margins.

2. Is the cruise industry in trouble?

No. Demand remains strong, but profitability is under pressure due to rising costs and external risks.

3. Which cruise stock is the best investment?

Royal Caribbean is currently the strongest performer due to better margins, pricing power, and execution.

4. Are cruise stocks a good investment now?

They can be, but they are volatile. Investors should be cautious and selective, focusing on balance sheets and operational efficiency.

Other personal finance blog posts