For a brief moment, HIMS stock looked unstoppable. Investors believed Hims & Hers Health had found the perfect business model: low-cost telehealth combined with booming demand for GLP-1 weight-loss drugs.

That optimism has collapsed.

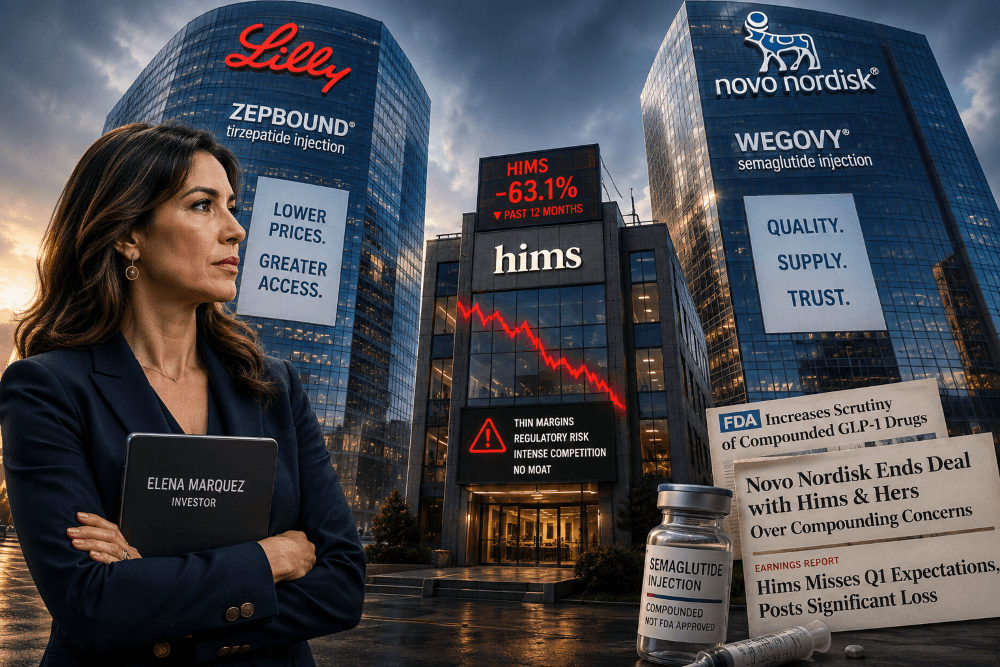

Today, HIMS stock is down roughly 63% over the past 12 months. The company recently posted disappointing quarterly results, missed expectations badly, and revealed just how fragile its business model may actually be.

At this point, HIMS no longer looks like a disruptive healthcare giant. Instead, it increasingly resembles hundreds of other telehealth companies operating on thin margins in a brutally competitive industry.

What Started the HIMS GLP-1 Boom?

The story began with GLP-1 drugs such as:

- Ozempic

- Wegovy

- Zepbound

These medications, developed by Novo Nordisk and Eli Lilly, became wildly popular for weight loss.

Demand exploded so quickly that shortages emerged across the United States.

That shortage created a legal gray area. Under certain conditions, compounding pharmacies are allowed to produce customized versions of drugs during supply shortages.

HIMS moved aggressively into this opportunity by partnering with compounding pharmacies and offering compounded semaglutide products directly to consumers through its telehealth platform.

Wall Street loved the idea.

Investors saw:

- massive demand

- subscription-based recurring revenue

- rapid customer growth

- and huge profit potential

For a while, HIMS became one of the hottest stories in healthcare investing.

The Problem: The Business Model Was Never Stable

The entire GLP-1 opportunity depended on a temporary market condition: shortages.

Once the FDA declared shortages resolved, the legal foundation supporting large-scale compounded semaglutide became much weaker.

That changed everything.

Suddenly:

- regulators increased scrutiny

- pharmaceutical companies pushed back aggressively

- and investors started questioning whether HIMS had any durable competitive advantage at all

The market began to realize that HIMS did not actually control:

- the drugs

- the patents

- the manufacturing

- or the supply chain

The company was simply acting as an intermediary.

That is a dangerous position when competing against trillion-dollar pharmaceutical giants.

Novo Nordisk and Eli Lilly Fight Back

Both Novo Nordisk and Eli Lilly responded aggressively.

They accused companies like HIMS of exploiting loopholes and marketing compounded products too aggressively.

At one point, Novo Nordisk briefly partnered with HIMS in an attempt to transition customers toward official branded products.

The relationship quickly collapsed amid public disagreements over compounded GLP-1 marketing practices.

Meanwhile, Eli Lilly began cutting prices and building direct-to-consumer distribution channels.

That may have been the biggest turning point of all.

If pharmaceutical companies can:

- manufacture the drugs

- lower prices

- sell directly to consumers

- and control fulfillment

…then what exactly is the long-term role of HIMS?

That question still hangs over the stock today.

HIMS Stock Is Now Facing a Reality Check

The latest earnings report exposed the pressure building underneath the surface.

The company:

- missed expectations

- posted significant losses

- and saw margins deteriorate sharply

This matters because telehealth is already a difficult business.

Many telehealth companies compete primarily on:

- convenience

- marketing

- customer acquisition

- and pricing

Those are not durable competitive advantages.

Without the GLP-1 growth narrative, HIMS increasingly looks like another online healthcare platform fighting for customers in a crowded market.

That is not the kind of business that typically commands premium valuations.

Why I Am Avoiding HIMS Stock

At current levels, HIMS may be able to stabilize temporarily.

However, I do not see a compelling reason to own the stock right now.

The company has several major problems:

- Thin margins

- Intense competition

- Regulatory uncertainty

- Dependence on pharmaceutical suppliers

- Lack of a clear moat

Most importantly, HIMS has not demonstrated a sustainable competitive advantage.

The market once treated HIMS as a revolutionary healthcare platform. Today, it looks much closer to a commodity telehealth provider.

Unless management develops:

- proprietary technology

- unique healthcare infrastructure

- exclusive partnerships

- or a differentiated service model

…the stock could remain dead money for a long time.

That does not necessarily mean the company is going bankrupt.

But there is a big difference between:

- surviving

- and generating strong shareholder returns

At the moment, HIMS appears to be stuck somewhere in the middle.

Could HIMS Recover?

Of course.

If the company successfully expands beyond GLP-1 products and builds a broader healthcare ecosystem, investor sentiment could improve.

But right now, the risks appear to outweigh the potential reward.

The original hypergrowth narrative has faded, and the market is still trying to determine what HIMS actually is.

Until that picture becomes clearer, I prefer to stay on the sidelines.

Final Thoughts on HIMS Stock

The GLP-1 saga transformed HIMS from a market darling into a cautionary tale.

For a short period, compounded semaglutide created explosive growth and investor excitement.

But once shortages ended and pharmaceutical giants responded aggressively, the weaknesses in the business model became impossible to ignore.

Today, HIMS faces:

- slowing momentum

- weaker margins

- intense competition

- and uncertain long-term positioning

At current prices, the stock may hold steady for a while.

However, without a meaningful competitive advantage, I believe HIMS risks becoming dead money for investors over the next several years.

Frequently Asked Questions

Why did HIMS stock fall so much?

HIMS stock declined because investors became concerned about regulatory risks, shrinking margins, and increasing competition in the GLP-1 market.

What are GLP-1 drugs?

GLP-1 drugs are medications used for diabetes and weight loss, including Ozempic, Wegovy, and Zepbound.

Does HIMS still sell compounded semaglutide?

HIMS has reduced some compounded GLP-1 offerings after increased FDA scrutiny and legal pressure from pharmaceutical companies.

Is HIMS profitable?

HIMS recently reported quarterly losses, raising concerns about the sustainability of its current business model.

Disclaimer: The information provided in this newsletter is for informational and educational purposes only. It does not constitute investment, financial, or legal advice. I am not a registered investment advisor. All “Buy,” “Hold,” or “Sell” ratings are expressions of personal opinion and should not be construed as recommendations to purchase or sell any security.

Other Stock Market blog posts