| 📊 Alain’s Holdings — June 10, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 667.05 | -10.65 | -1.57% |

| QQQ | Invesco QQQ Trust | 693.69 | -14.14 | -2.00% |

| XIU.TO | iShares S&P/TSX 60 ETF | 50.72 | -0.25 | -0.49% |

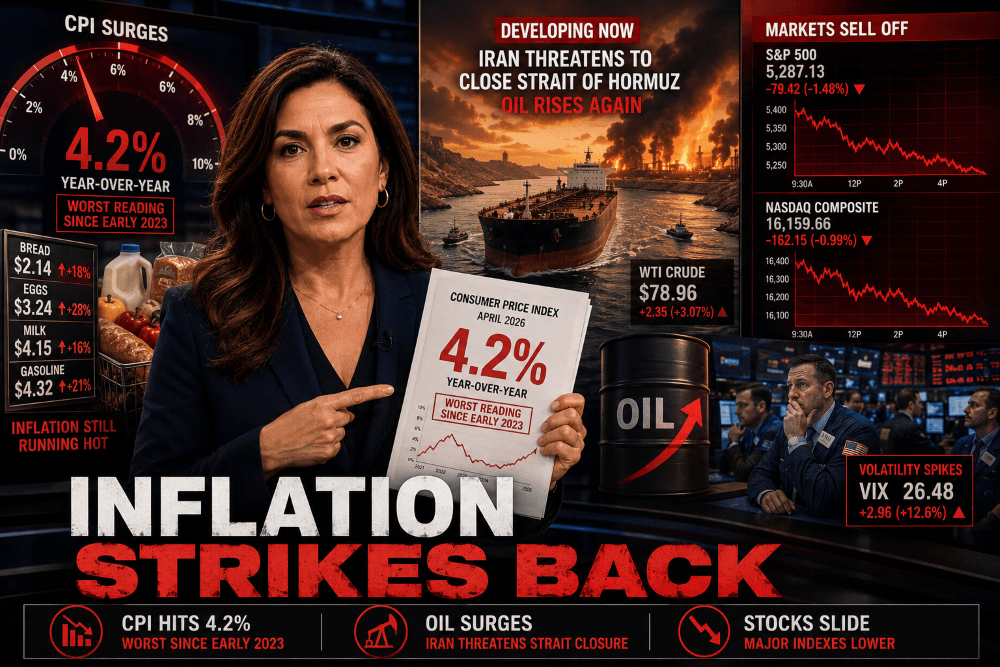

Inflation Hits a 3-Year High.

Oracle Declins.

May CPI came in at 4.2% year-over-year — the worst reading since early 2023 — sending stocks lower all session. Oil rose again as Iran threatened to completely close the Strait of Hormuz. Then Oracle reported record quarterly results after the bell, But decliened 4% in after-hours trading and offering a timely reminder that the AI infrastructure buildout is very much alive. SpaceX priced its historic IPO at $135/share.

Index Close

S&P 500

7,348.85

Nasdaq Composite

25,520.98

Dow Jones

50,573.49

Russell 2000

~2,880

Market Snapshot

The Trigger — May CPI Report

4.2% Year-Over-Year — A 3-Year High Fueled by War

May’s CPI report confirmed what markets feared: headline inflation jumped to 4.2% year-over-year — its highest reading since early 2023 and a sharp acceleration from April’s already-alarming 3.8%. The monthly gain of 0.5% was driven almost entirely by energy costs, reflecting the Iran conflict’s sustained chokehold on the Strait of Hormuz and global oil supply. The one saving grace: core CPI (excluding food and energy) rose just 0.2% month-over-month, below the expected 0.3%, suggesting that inflation’s momentum is war-driven rather than broadly entrenched. JPMorgan’s economics team noted May may be “peak” headline inflation if a Hormuz deal is reached — but that is a conditional forecast. The Federal Reserve, now holding its rate at 3.50%–3.75% after three consecutive pauses, faces an impossible choice: act on headline inflation and risk recession, or hold and watch energy-driven price pressures erode household purchasing power through summer.

Record Quarter: $19.2B Revenue, Cloud Up 47%, IaaS Up 93% — Shares -4% AH

Oracle delivered one of its strongest quarters on record. Total revenue of $19.2 billion exceeded the $19.1 billion consensus, growing 21% year-over-year. Cloud infrastructure (IaaS) revenue surged 93% as Oracle’s massive $553 billion contracted backlog — representing eight times annual revenue — began converting into recognized revenue at an accelerating pace. Cloud applications (SaaS) grew 10%. Non-GAAP operating income rose to a record $8.6 billion, up 22%. The company confirmed its FY2027 revenue target of $90 billion and raised non-GAAP EPS guidance to $8.05 — growth of 18% year-over-year. CEO Safra Catz cited “dramatically higher” growth ahead. Shares surged approximately 11% in after-hours trading, erasing a week of losses in a single session. The Oracle result is a direct rebuttal to the post-Broadcom narrative that the AI infrastructure trade is stalling: the backlog is real, the conversion is happening, and enterprise AI demand is accelerating.

What Happened Today

The session began and ended with inflation. The 8:30 AM CPI print — 4.2% year-over-year — landed exactly in line with expectations, which meant stocks showed “little net reaction” immediately after the release, according to multiple analysts. Markets had already priced in a hot number after Monday’s Iran helicopter incident reignited oil fears. But “in-line” at a 3-year high still meant no relief: the 10-year Treasury yield held stubbornly near 4.56%, rate-cut odds remained near zero, and the market’s prevailing mood was cautious to negative throughout the session.

Iran raised the stakes further. Tehran announced it was ceasing negotiations with the U.S. and threatened the complete closure of the Strait of Hormuz, sending oil prices spiking again toward $96+ on Brent. The International Energy Agency responded with an emergency authorization: a record release of 400 million barrels of oil from member nations’ strategic reserves — surpassing its previous record action in 2022. The IEA move partially cooled the immediate oil price spike, but the structural problem remains: so long as the Strait is threatened, inflation has a floor that monetary policy cannot easily lower.

The AI equity dilution wave continued. Super Micro Computer (SMCI) fell approximately 18% after announcing a $7 billion equity raise to fund its $39 billion AI server order backlog — extending Tuesday’s 9.5% drop for a combined two-day loss of roughly 26%. The move raised fresh questions about the financing sustainability of smaller AI infrastructure suppliers. In sharp contrast, Dell Technologies rose 4% — the market’s verdict was clear: cash-flow-funded AI winners (Dell) are preferred over debt-and-dilution-funded ones (SMCI). Meanwhile, Alphabet’s raise was confirmed to have been upsized to $84.75 billion, and reports surfaced of upcoming IPOs from Anthropic and OpenAI — suggesting the AI capital arms race has no near-term ceiling.

SpaceX priced its IPO at $135 per share, the top of its range, after drawing more than $250 billion in investor demand — more than three times the $75 billion it sought to raise. That extraordinary demand signals that despite the broader market volatility, institutional appetite for the biggest AI-adjacent IPO in history remains intact. SpaceX begins trading Thursday on the Nasdaq under the ticker SPCX.

The Russell 2000 outperformed for the fifth session in the past six, gaining 0.41% while large-cap indexes fell. Nine of eleven S&P 500 sectors actually advanced during the session — but the sheer weight of mega-cap tech declines pulled the headline indexes negative. This is an increasingly important nuance: the broader U.S. market is holding up; it is concentrated tech and AI-hardware names that are dragging the tape.

The AI Server Trade Splits in Two

Notable Movers

📈 Winners

📉 Losers

💰 The AI Capital Raise Wave — 2026 Scoreboard

| Company | Purpose | Amount |

|---|---|---|

| Alphabet (GOOGL) | AI infrastructure capex | $84.75B (upsized) |

| Meta Platforms | AI infrastructure capex | Multi-billion (pending) |

| SpaceX (SPCX) | IPO — Starlink + AI infra | $75B raise · $1.75T valuation |

| Super Micro Computer | AI server component purchasing | $7B equity raise |

| Oracle | AI data center buildout | $30B (Feb) + $45–50B planned |

₿ Bitcoin — Down Again: ~$61,697 (−1.33%) · 8th Down Day in 10

Bitcoin fell another 1.33% Wednesday, closing near $61,697 — its eighth losing session in the past ten trading days. The pattern is unambiguous and entirely consistent with what a speculative asset with no intrinsic value does during periods of rising inflation, elevated interest rates, and geopolitical uncertainty. Headline CPI at 4.2%, a 50% market-implied probability of a Fed rate hike, and Iran threatening to close the Strait of Hormuz are not conditions that support assets with no earnings, no cash flows, and no physical backing. Bitcoin’s year-to-date loss now stands at approximately 13%, and it sits roughly 50% below its all-time high. Strategy Inc.’s continued Bitcoin purchases have failed to arrest the slide. When macro conditions are this hostile to speculation, there is simply no fundamental anchor to prevent further declines.

🚀 SpaceX IPO — Priced at $135/Share · Lists Tomorrow on Nasdaq (SPCX)

SpaceX priced its IPO at $135 per share — the top of its range — after generating more than $250 billion in investor demand for a $75 billion offering. That is more than 3x oversubscribed. At $135/share the implied valuation is $1.75 trillion, ranking SpaceX among the ten most valuable companies in the world on its first day of trading. The deal’s extraordinary demand — even in the midst of the worst week for tech stocks since April 2025 — confirms that institutional appetite for generational AI-adjacent companies remains intact regardless of short-term volatility. Retail investors who registered interest via Robinhood and SoFi will receive their allocation notices tonight. Trading begins Thursday morning under SPCX on the Nasdaq.

What to Watch Tomorrow — Thursday, June 11

- SpaceX (SPCX) first-day trading: The most anticipated market event of the year begins Thursday morning. At $1.75T valuation, every tick will be watched globally. A strong first-day pop confirms risk appetite. A disappointing open or early selling would signal that even the most hyped IPO in history cannot escape the current macro headwinds.

- Oracle (-5% AH) open: ORCL’s record results should translate to a significant gap-up at Thursday’s open. Watch whether the move holds — a sustained Oracle rally would meaningfully help stabilize the Nasdaq after a week of semiconductor pain.

- Adobe earnings (after close): Adobe reports Q2 with a $25 billion buyback authorization in its back pocket. The AI-replacement narrative has hit software stocks hard — Adobe’s guidance will be a key read on whether creative AI is cannibalizing or augmenting its core franchise.

- May PPI (8:30 AM ET): The producer price index will reinforce or soften Wednesday’s hot CPI read. A soft PPI would confirm that inflation pressures remain energy-driven and potentially peaking. A hot PPI would accelerate rate-hike expectations further.

- Iran/Hormuz: Tehran’s threat to completely close the Strait is the single biggest tail risk for markets right now. Watch crude futures and any diplomatic response from the U.S. before Thursday’s open. The IEA’s 400M barrel reserve release provides a temporary buffer — but it is not a permanent solution.

Other Stock Market blog posts