| 📊 Alain’s Holdings — June 9, 2026 | ||||

|---|---|---|---|---|

| Symbol | Name | Price | Change | Change % |

| VOO | Vanguard S&P 500 ETF | 677.70 | -2.08 | -0.31% |

| QQQ | Invesco QQQ Trust | 707.83 | -8.24 | -1.15% |

| XIU.TO | iShares S&P/TSX 60 ETF | 50.97 | -0.01 | -0.02% |

One Step Forward,

One Helicopter Back

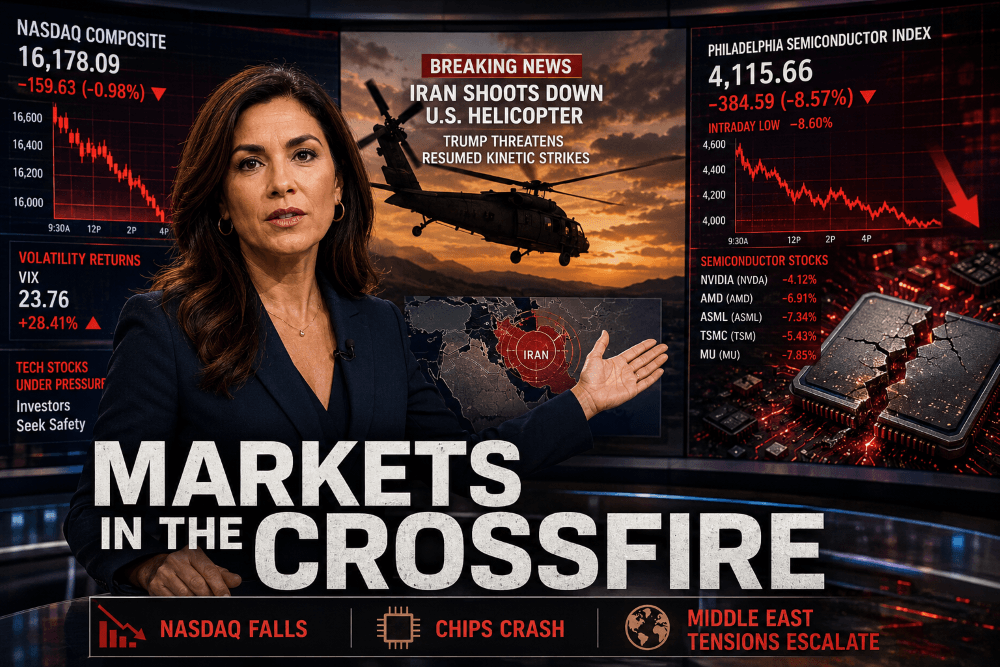

Monday’s relief rally evaporated in hours. Iran shot down a U.S. helicopter, Trump threatened resumed kinetic strikes, the Nasdaq plunged nearly 1%, and the Philadelphia Semiconductor Index cratered 8.6% intraday before a partial recovery. Markets closed mixed in one of the most volatile sessions of the year — with trillion-dollar events lining up for Wednesday.

Index Close

S&P 500

7,386.65

Nasdaq Composite

25,678.82

Dow Jones

50,872.11

Russell 2000

~2,863

Market Snapshot

The Intraday Whipsaw

⏱ How Tuesday’s Session Unfolded

Notable Movers

📈 Bucking the Trend

📉 Under Pressure

What Happened Today

The market gave back Monday’s optimism in real time. The session opened on a constructive note — chip stocks were rallying, the tape looked stable, and Monday’s Iran de-escalation narrative appeared to be holding. Then, mid-session, reports emerged that Iran had shot down a U.S. military helicopter. Trump’s post threatening that the U.S. “must react” immediately triggered a violent sell-off. The Philadelphia Semiconductor Index swung from +3% to −8.6% intraday — one of the most dramatic single-session reversals in recent memory for the chip sector.

The Strait of Hormuz returned to center stage. Iran’s effective closure of the Strait — a route for approximately 20% of global oil, fertilizers, and other key commodities — has become the single most consequential variable for inflation in 2026. In April, CPI hit 3.8% year-over-year, its largest annual gain in nearly three years, driven partly by a 28%+ surge in gasoline. With the May CPI report due Wednesday, the helicopter incident added fresh concern that inflation data will again print hot, further eliminating any prospect of Fed rate cuts and potentially reigniting rate-hike fears. Markets are currently pricing in a roughly 50% chance of a Fed rate hike by year-end — a remarkable shift from early 2026 expectations of multiple cuts.

The rotation continued regardless. Even as tech sold off violently intraday, the Dow and Russell 2000 finished green. Nine of eleven S&P 500 sectors closed positive. Consumer staples, healthcare, financials, and utilities all outperformed — a pattern now five sessions old. Market strategist Michael O’Rourke of JonesTrading captured the dynamic well: “When the bounce ran its course this morning, the tape came for sale more broadly. There’s also a rotation going on… so part of it is more of a momentum unwind.” The Russell 1000 Value index outperformed the Growth index for the fourth consecutive day.

SpaceX portfolio rotation is also a factor. Several strategists noted that investors may be trimming high-flying semiconductor positions to make room for SpaceX in their portfolios ahead of Thursday’s debut. The IPO is reportedly oversubscribed and is pricing Wednesday evening — and at a $1.75 trillion valuation, even a modest allocation from institutional investors requires selling something else first. With the semiconductor index still up over 70% year-to-date despite the recent selloff, chips are the logical source of funds.

Apple kicked off WWDC but the opening keynote produced mixed initial reactions — with reports that Apple shares dropped after the conference opened. Details on the degree of AI integration and any new subscription-tier announcements are expected throughout the week. The market will be closely watching for any Siri monetization or third-party AI model integration news that could justify Wedbush’s bullish $400 target.

Economic Data & Geopolitical Risk

📊 NFIB Small Business Optimism — May 2026

Missed the 96.0 consensus. Small business sentiment fell in May as owners cited unpredictable fuel price spikes from the Iran conflict as a major challenge — one they find harder to pass on to customers than large corporations. The share of owners planning to raise prices over the next three months climbed to its highest level in nearly four years. NFIB Chief Economist Bill Dunkelberg noted that AI investment has generated “excitement” — but the overall picture is divided. Inflation expectations at the small business level are rising again.

🛢️ Strait of Hormuz — The Inflation Choke Point

Iran’s effective closure of the Strait of Hormuz is disrupting roughly 20% of global oil flows, fertilizer, and commodity shipments. The conflict has pushed a broad commodity index up 40.5% year-over-year. Reports of multiple explosions near Bandar Abbas — on the coast of the Strait — emerged Tuesday evening. Even a partial reopening after a deal would immediately ease energy price pressures. Trump said the Strait would reopen “immediately” after any agreement with Iran — making a deal the single most deflationary event that could happen to markets right now.

Wednesday: Three Market-Moving Events in One Day

📊 May CPI — 8:30 AM ET

The most important inflation reading since April’s shock 3.8% YoY print. Consensus expects headline CPI around +0.3% MoM. A hot number would reignite rate-hike fears and could push the Nasdaq another 2–3% lower. A soft number could spark a sharp relief rally across tech and bonds.

🚀 SpaceX IPO Pricing (SPCX)

SpaceX prices its $75B raise at $135/share Wednesday evening, targeting a $1.75T valuation for Thursday’s Nasdaq debut. Oversubscribed. If the deal prices above expectations, it confirms institutional risk appetite. If it stumbles, it could accelerate the current tech/chip selloff.

🔮 Oracle Earnings — After Close

Oracle reports Q4 results with consensus EPS of $1.96 (+15.3% YoY). All eyes on cloud revenue growth and AI infrastructure backlog guidance. A beat and raise could restore confidence in the AI capex story that Broadcom’s miss shook. A miss would compound the damage.

₿ Bitcoin — ~$63,300 · Marginal Gains in a Volatile Session

Bitcoin continued its downward slide, hovering around $61,600 — about 2.8% below Monday’s close, and still down approximately 13% from its pre-selloff level of ~$70,800 at the start of last week. Strategy Inc. attempted to calm markets by disclosing it had purchased 1,550 BTC for approximately $101 million — far more than the $2.5 million it previously sold. The buy was framed as a reaffirmation of conviction, but market confidence has been slow to recover. As we have noted throughout this week: Bitcoin remains a speculative asset with no intrinsic value. It produces no earnings, generates no cash flows, and holds no physical backing. Its partial recovery this week tracks the broader risk-on/risk-off cycle driven by Iran headlines — not any change in fundamentals, because there are none.

What to Watch Tomorrow — Wednesday, June 10

- May CPI (8:30 AM ET): This is the most consequential data point of the week — possibly of the month. After April’s 3.8% YoY print and the NFP shock last Friday, markets are walking a tightrope. A hot number (above +0.4% MoM) could push the S&P 500 below 7,300. A soft number (below +0.2%) could trigger a sharp Nasdaq relief rally and reset the tone heading into the SpaceX IPO.

- SpaceX (SPCX) IPO pricing: Pricing is expected Wednesday evening ahead of Thursday’s open. The deal’s final valuation ($1.75T vs. potential upsize to $1.8T+), allocations, and early grey-market trading will set the tone for Thursday’s debut — and for market risk appetite broadly.

- Oracle earnings (after close): CEO Safra Catz’s guidance on cloud backlog and AI-driven demand will be scrutinized as a health check for the enterprise AI spending cycle. Oracle has reported strong cloud growth in recent quarters — a beat could help stabilize chip sentiment by validating the AI capex thesis.

- Iran/Hormuz overnight: Reports of explosions near Bandar Abbas and Trump’s “must react” language mean the overnight news flow matters enormously. Watch crude oil futures and S&P 500 futures before Wednesday’s open for real-time geopolitical signals.

- Apple WWDC (Day 2): After an apparently mixed first day, Wednesday’s sessions could include deeper AI announcements. Any meaningful Siri/AI integration news has the potential to be a standalone positive catalyst for AAPL, which has been largely absent from the current tech selloff narrative.

Other Stock Market blog posts